CERTIFIED FINANCIAL PLANNER™ Loren Merkle discusses the crucial mindset shifts needed when rethinking retirement income. He emphasizes the importance of understanding how retirement income works and strategies needed to navigate this phase of life, including:

– The downfall of using Rules of Thumb in retirement planning

– The upside of controlling your own paycheck in retirement

– The Importance of using Social Security options to your advantage

–––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

TRANSCRIPT

Molly Nelson [00:00:02]:

What do you do when the employer paycheck goes away in retirement? You have to rethink income. We show you how right now on Retiring Today. This is Retiring Today. I am here with Loren Merkle. He is a CERTIFIED FINANCIAL PLANNER™, a Certified Financial Fiduciary®, and a Retirement Income Certified Professional®. Loren, every day you sit down with people, and they’re getting ready to retire. They’re excited, but they also have to kind of get ready for a bit of a mindset shift.

Loren Merkle [00:00:38]:

They’re excited, and the conversations are a lot of fun because we think about what’s on the other side. But you’re right. The things that we think about, retirement planning and all the decisions we think we have to make and the answers we have to come up with, oftentimes, reality looks a lot different, and there’s a lot of different reasons for that, whether it’s the studies that we read or things that we hear on the news or what our coworkers experience were or maybe even siblings experiences were. We find out what is, what is our decision-making process, and the outcomes can be, and most likely will be different. And that does require a different way of thinking about making that transition.

Molly Nelson [00:01:17]:

Today, we want to focus on income, but we’ve put together a whole series of workshops on this concept, because there are a lot of things you have to rethink as you get closer to retirement. There’s a website on your screen right now. It’s our RethinkRetirementSeries.com. And that’s where you can go look into all of these workshops that we’ve put together. Hey, let’s focus on income, because before we can rethink retirement, let’s get a really clear picture of where people are at before retirement. So they’re getting a steady paycheck. It’s pretty predictable when it comes to.

Loren Merkle [00:01:46]:

Income, it’s predictable as long as you’re employed, you know the employer’s gonna continue to pay you. Maybe every year, we get a little bump in what that pay is going to be. So your income is largely supplied by the day to day efforts that you put into your employment. When you retire, that employer is no longer going to pay you because you’re no longer working. And now your retirement paycheck is going to be largely dependent upon how you construct the income resources that you have. Some people still have a pension, so that could be a part of that. Some people, most people have Social Security. That can be a part of that.

Loren Merkle [00:02:22]:

Now it’s digging through the nuances of all the different Social Security options that may be available to you. And then many people do have investable assets, and that is a big challenge for, for many people to now think about how is, how are you going to take money out of these investable assets instead of putting money into them like you probably have been for the last 40 years?

Molly Nelson [00:02:43]:

I’m glad you said pensions, because it really wasn’t that long ago, I think I recently read that in the 1980s, 60% of private sector workers were offered pension plans. By 2020 or 2022, that number was 4%. So now, people, it’s on people. It’s a lot more difficult for this generation to figure out retirement income than it was for your grandpa, who retired from Ford Motor Company.

Loren Merkle [00:03:05]:

If we were sitting here in the eighties when my grandpa retired, we would be talking about this concept called the three legged stool, where you had your pension, you had Social Security, and maybe you had a little bit of savings, which is exactly how my grandpa retired. My grandpa worked at Ford Motor Company for 40 years. He retired in his mid-fifties, and then grandma and grandpa traveled around the country in their motor home. They had a wonderful full retirement. There’s a couple summers that. That myself and my brothers, brothers and sister got to go with them. It was a lot of fun. They had pension from Ford Motor Company, Social Security, and then a little bit of savings.

Loren Merkle [00:03:43]:

It worked really well. If grandpa was retiring today, it would be substantially different, because most people, as you alluded to, Molly, don’t have one of those core tenets of the income, that pension. So now it’s going to be Social Security and the investable savings, which is going to make up the bulk of. Of the retirement income. And one of the problematic aspects of what the environment people are retired in today is the uncertainty of how long are you gonna live? How much money do you need to live on? When my grandpa retired, he didn’t have to answer the question, how much money does he need to live on? He was living on the income coming in, the pension and the Social Security income. Now you have to determine how much money can you spend now, today, and still have confidence that you’re not going to run out of money before you run out of time.

Molly Nelson [00:04:30]:

Yeah. And when you have a pension, you have maybe a couple of options of how to take that money. When you have a 401(k) or a 403b, and then you leave retirement, you’ve got all kinds of options with what to do with the money, where to take it from, how to take the money. It’s just a lot to figure out.

Loren Merkle [00:04:43]:

It’s a lot to figure out, and there’s a lot of strategies out there that people write about and talk about that you can get easily mixed up with. How do those strategies work? Do they work? Should they work like the 4% rule? You know, you take your Social Security, you have a million dollars in your investable assets. Let’s take 4% out of your million dollars of investable assets, which means that’s $40,000 of income, and maybe increase that each year with inflation, and that will sustain for the next 20, 30, 40 years, maybe. But how do you really know?

Molly Nelson [00:05:13]:

Yeah, that’s one of those rules of thumb. I think if you look up retirement income, that one comes up. Another thing I read a lot is you need $1 million, $2 million, $3 million to retire. That gets confusing for people as they’re trying to make sense of this.

Loren Merkle [00:05:25]:

I was in a visit recently, and I was working with an individual, and we got done with his plan, and he wants to retire at the end of the year, spend about $6,000 a month. And we showed him where the income was going to come from, how long that was going to last. He’s age 100. When he’s age 100, he still has plenty of money left over. So there should not be a real concern of him running out of money. But we got done reviewing the plan, and he kind of sat back and he was like, so I don’t need $3 million to retire? No, I said, what? He goes, I don’t need $3 million? I read I needed $3 million in order to successfully retire. And that’s all the type of information that you have to sort through to determine, is that applicable to me? Do I need $3 million to retire? What does that really look like? The fact is, most people in this country retire with far less than $3 million, and they have a fantastic, or can have a fantastic retirement.

Molly Nelson [00:06:22]:

Okay. I think we’ve done a good job of outlining some of the concerns that people have and some of the stuff that they’re hearing when it comes to retirement income. So ready to shift some minds here?

Loren Merkle [00:06:31]:

Let’s shift it.

Molly Nelson [00:06:31]:

Have people rethink retirement to put them in a better position. So what mindset shift number one we want to talk about today is taking Social Security. I think a lot of people think the day I retire is the day I take Social Security.

Loren Merkle [00:06:43]:

Yeah. Because we do read a lot of articles that say, let’s take it right away, as soon as you possibly can, which for most people is age 62. So if you retire at 62. You know, you’re eligible for this benefit you’ve been paying into for the last 40 years, and you’re like, okay, it’s time to get some money back. Especially when you see the studies that say by the year 2032 or 2034, Social Security is gonna go broke or be reduced by 25%. You know, you hear and see all of those different things. So you’re thinking, and should I take it? Should I not take it? On the other side, you see articles that say you need to wait as long as you possibly can, because from your full retirement age all the way up until 70, you get an 8% guaranteed increase on lifetime income. So you would be crazy not to wait as long as you can.

Loren Merkle [00:07:33]:

And so there’s all these different types of thoughts around Social Security. And when you really look into it, you have up to 81 different options when it comes to selecting Social Security. So how do you know which of those 81 different options is right for you? And if you’re married, then you have even more options, and it can be even more complex.

Molly Nelson [00:07:53]:

I didn’t want you to give me more choices. I wanted you to narrow this thing down for me. I don’t necessarily have to take Social Security the day that I retire, but generally. Are you saying it’s across the board? Some people take it a lot longer after the trial. Some people wait till 70, some people 65. Cause I’m thinking 65 is a number a lot of people get fixated on.

Loren Merkle [00:08:11]:

There’s a lot of factors that go into when you should take your Social Security. It’s going to be your health status, because that’s going to directly impact your life expectancy, which is going to directly impact the return on your Social Security investment. It’s going to be your cash flow requirements, not only at retirement, but maybe 5, 10, 15 years into retirement. What those projections look like, it’s also going to be dependent upon what other income sources do you have. Do you have a pension? How much investable assets do you have to also deliver income? So we look at all the different income levers that you have, whether it’s your pension, certainly Social Security and investable assets. And then we determine, based on all these other factors, cash flow, life expectancy, et cetera, this would be the best time for you to take your Social Security. And here’s the strategy of what that looks like. And then one of the things we do for the families that we work with is we will file those Social Security benefits for them.

Loren Merkle [00:09:06]:

Cause that’s one of the overlooked aspects of Social Security okay, you know what you want to take now you have to go get it done.

Molly Nelson [00:09:12]:

Yeah, I’m sure. I’m just guessing. It’s not super easy.

Loren Merkle [00:09:16]:

It can be difficult. Now. It’s easy for us because we do it over and over and over. You can file online, and there’s some nuances and complexities to that. You can call them. It used to be you could go down to the Social Security Administration to file in person. They really don’t like that much anymore. So there’s different ways you can do it.

Loren Merkle [00:09:33]:

But because we do it over and over and over, it’s much easier for the families and individuals that we serve, for us just to do it.

Molly Nelson [00:09:39]:

And here’s what I liked. I heard you say the 81 different options, but you were able to narrow it down. It started up here and we were able to get here. If we answer a few questions, we look at a few factors in your life, we really can help you make the decision that will maximize this benefit for you.

Loren Merkle [00:09:52]:

Yeah, nobody wants to look at all 81 different options. That’s our job. So what we do is we take all the factors into consideration and narrow the 81 different options down to a manageable subset and say, here’s maybe your top five options. And if you elected this option, here’s how it would impact your short term retirement plan and your long term retirement plan. But what if you made this decision? Here’s how it would impact short term, long term. And then once you see the real outcome, short and long term, that Social Security decision becomes way easier than it was on the onset.

Molly Nelson [00:10:29]:

So you may be wondering, how will your Social Security decision impact you? You can talk directly with a retirement planner about it. Schedule a 15 Minute Retirement Check-Up Call right now by going to MerkleRetire.com right now. There’s a calendar. You can choose a time and a date that works for you and talk about Social Security or anything that is on your mind when it comes to retirement. Two more ways to rethink income in retirement. Next.

Voice Over [00:11:04]:

You dream of a happy retirement. But there are some big questions to answer. First, do I have enough saved? When should I take Social Security? How will I pay for health care and keep up with inflation? Go to MerkleRetire.com to schedule a 15 Minute Retirement Check-Up Call to talk directly with a retirement planner and get answers to your important retirement questions. The first step to your retirement starts with a 15 Minute Retirement Check-Up Call.

Voice Over [00:11:34]:

Anytime I have even the smallest question about my accounts or what effect the latest tax law might have on my situation. The Merkle Retirement Planning team is always there and quick to help. I’m so glad they treat you like. Well, like family. I’m so happy to have such an excellent team working for my future and ensuring I do the best to achieve my financial goals.

Voice Over [00:11:58]:

Merkle Retirement Planning. Your retirement starts here.

Molly Nelson [00:12:15]:

I’m here with Loren Merkle, and this is Retiring Today. Welcome back. We are talking about why retirement is a mindset shift. Our first mindset shift was we’re talking about taking Social Security, rethink Social Security. Our next mindset shift is don’t use rules of thumb. Loren, you talked about it when you look up retirement information. There are a lot of rules of thumb out there, and you caution people on using those when it comes to planning a 20 or 30 year retirement.

Loren Merkle [00:12:38]:

But it’s so tempting, Molly, especially when we’re doing something we’ve never done before, like deliver income that we, our lifestyle is dependent on from our investable assets. 4%. I got a million dollars in my portfolio. 4%. That’s $40,000. That’s easy math. I can do that. The problem with that is that may work out, but it also may not work out.

Loren Merkle [00:13:00]:

And when we’re talking about your lifestyle for the rest of your life, 20 to 30 years, you want to be as certain as you possibly can that it will work out. What do we mean by that? Let’s say you are employing that 4% rule. You have a million dollars. But we go through a really poor market cycle, kind of like what we did at the turn of the century. The year 2000, the market was down. 2001, the market was down. 2002, the market was down, which is why a lot of people had to come out of retirement or postpone their retirement if they were dependent upon a rule of thumb, like the 4% rule. And then we take the next decade, 2010.

Loren Merkle [00:13:38]:

Well, we just came off the heels of 2008. A lot of people didn’t recuperate from 2008 for maybe five, six, seven years. So now we’re looking at 2015, 2016, 2017 before they were back to even, let alone making money. And that could work. The 4% rule could work in that type of decade. But here we are in another decade, and the market is all over the place, bouncing all over the place. And the 4% rule doesn’t account for that market variation because the 4% rule is based on a stock bond portfolio with some kind of assumed rate of return. But it’s not accounting for what happens if the market goes down 30%.

Loren Merkle [00:14:19]:

The average portfolio in 2022 of 401(k) plans, I think it was. According to Fidelity, said the average 401(k) plan was down 23%. If you’re retired, depending upon income, your portfolio is down 23% and you’re taking money out to live on. Something has to give. So it’s either your lifestyle, you have to take less out, or you’re running the risk of running out of money before you run out of time.

Molly Nelson [00:14:42]:

When I read about these rules of thumb two, they talk about taking some certain amount out again, whether it’s 4%, 3%, 5%. And when I look at it, I think, well, spending isn’t a straight line in retirement. I mean, you know that better than anyone else. You help people spend and save all the way through and invest through retirement. It’s got its ups and downs.

Loren Merkle [00:15:00]:

Yeah, you set your budget for retirement. Let’s say you think your lifestyle over the course of your retirement, or at least when you start, is going to be $6,000 a month. Well, that’s just your expenditures on a monthly basis. That does not usually account for, you have to replace a car, maybe you have to replace a couple cars, maybe you replace a roof. It doesn’t typically account for those one time bigger expenses, which you have to account for some way somehow. So again, incorporating that 4% rule, you have a million dollars, you’re taking 4% out. Even if the market’s doing okay, that will account for your monthly expenditures. But what are you going to do when you need $40,000 for the new car? Because that will deplete from the million dollars, and maybe the market won’t catch up with that depletion of the account.

Loren Merkle [00:15:46]:

And that’s in an okay market. We go through a really poor market, and this is what creates, or at least adds to a lot of the fear, a lot of the concern of retirees, because you really get one shot to get it right. And a lot of these decisions that you have to make, like what strategy you’re going to take, what strategy you’re going to use to take money out of your portfolio. At some point, you don’t have another shot to get that right. There is room for some mistakes, but you can’t make really big mistakes where it will have a lasting impact probably for the rest of your life.

Molly Nelson [00:16:20]:

So I have a pretty good understanding of why I don’t want to use rules of thumb when it comes to my retirement. But what do I want to use? How do I plan for income in retirement?

Loren Merkle [00:16:28]:

This is where the customization comes into play because, and think about it from the standpoint that this is your retirement. It’s not your neighbor’s retirement, it’s not your coworker’s retirement. It is definitely not your parents retirement. This is your retirement. So you should employ strategies that are right for you and the type of retirement that you want to live. Retiring today is a lot, a little bit different for everybody. It’s not like when my grandpa retired, where people collect Social Security and pension and they just did what they did. A lot of people today will phase into their retirement.

Loren Merkle [00:16:59]:

Well, they’ll stay at the same company, but instead of working 50 hours a week, maybe it’s 30 hours a week, some people will leave their career, that they’ve been in for the last 20 to 30 years, and they’ll work part time doing something completely different. Or they’ll emphasize volunteer work, where all of that is going to require a different set of planning, not necessarily principles, but strategies and tactics to account for what you want your lifestyle to look like, what you really want to accomplish and deliver you purpose as you go to and then through your type of retirement.

Molly Nelson [00:17:32]:

And when you were talking about some of your concern with the four percent rule and you were talking about the markets, I was kind of thinking too, that would happen to people when their portfolios are down, if they were heavily invested in the market or maybe too heavily invested in the market. My point being that customization is maybe having some money in the market, but maybe in some other spots that are a little less risky.

Loren Merkle [00:17:51]:

Yeah, that’s the other consideration we haven’t even talked about yet. We’re talking about taking money out, but that’s going to directly influence how you invest your portfolio, which is what a lot of people haven’t considered before. When you’re working, putting money into your 401(k), in your IRA, you can take a lot of risk because you have more time frame and your lifestyle is not dependent upon taking money out of that now. Your lifestyle is dependent upon it. And when the market is down, and we know the market goes up and it goes down, on average, we go through recessions every five to six years. So hopefully over the course of your retirement, you will live through four to six different recessions. That’s just inevitable, hopefully. But now you have to survive them.

Loren Merkle [00:18:36]:

Your portfolio has to survive them and still provide the lifestyle income that you require, which will require a different type of investment strategy than you’ve ever had to employ before. When you’re working just a 60/40, 70/30 portfolio, right. 70% of your investments in stock 30% of your investments in bonds. That can work through the ups and downs. When you’re retired needing income now, you have to get a little bit more creative, be way, way more intentional. And it does help to incorporate other types of investments than just stocks and bonds. You can incorporate alternatives into the portfolio that will react differently than stocks and bonds in the same economic condition. And why is that important? Because your lifestyle income is of the utmost important to make sure you can still maintain that lifestyle that you’ve always dreamt of.

Molly Nelson [00:19:30]:

Loren, it’s almost like you have to rethink everything in retirement. So you’re talking about rethinking income and you’re talking about rethinking investments. I’m guessing there’s some other things we have to rethink as well.

Loren Merkle [00:19:39]:

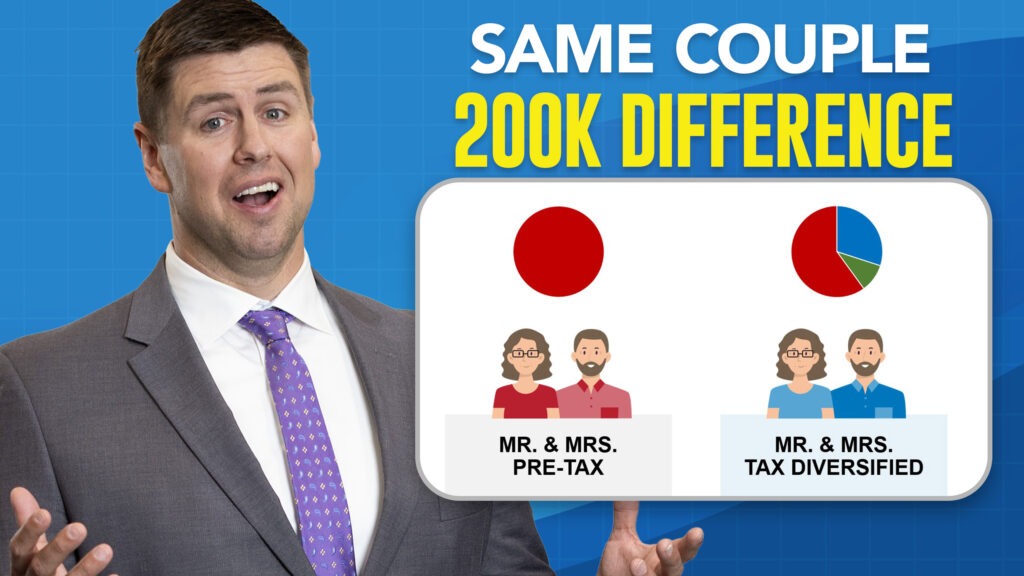

Rethink what’s going to happen to the portfolio or anything, any of the assets that you have once you do pass. Do you want some of it to go to charities? Do you want it to go to kids? Grandkids? What do you want that legacy to look like? You have to rethink your tax strategy because when you’re working the income, the w two income you have coming in that was taxed at ordinary income when you’re retired, you can create tax diversification where income from your Social Security may be not taxed as much. Income from Roth IRAs are not taxed at all, income from 401(k). So you have more opportunity to create tax diversification, which means you have opportunity to decrease your overall tax bill, not only on an annual basis, but certainly over the course of your retirement.

Molly Nelson [00:20:25]:

There is a theme here. It’s rethinking retirement, and there’s a lot that you have to rethink as you get closer to retirement. Here’s a great resource for you. It’s our rethink retirement series workshops. You can go to RethinkRetirementSeries.com right now and sign up for those workshops and go in depth with some of these topics that Loren was talking about. Taxes, health care, legacy planning. We’ve still got one more topic to tackle when it comes to rethinking retirement and income. Next.

Voice Over [00:20:55]:

Do I have enough saved for retirement? When should I take Social Security? Which Medicare option is best? How do I plan for inflation? Sometimes the road to retirement starts with more questions than answers. We’re here to help. Join us for our upcoming Journey to Retirement workshops. Get answers and start your retirement journey with confidence. Our online workshop includes information on Secure Act 2.0 and changing retirement rules. Visit RetireWithMerkle.com to register for an upcoming workshop. Your retirement journey starts now.

Voice Over [00:21:26]:

The Merkle Retirement Planning team provides personable and professional expertise unrivaled in this area. They include us in every step of the planning process. The peace of mind provided to us by the Merkle team allows us to fully enjoy this special time of our lives. Instead of feeling snake bit, we feel confident that with the Merkle Retirement Planning team at our sides, we can navigate any challenge that comes our way.

Voice Over [00:21:51]:

Merkle Retirement Planning. Your retirement starts here.

Molly Nelson [00:22:06]:

Welcome back to Retiring Today. I’m here with Loren Merkle, and we are talking about mindset shift number three when it comes to retirement income. And that shift, Loren, is know your numbers.

Loren Merkle [00:22:15]:

The numbers are, is what’s going to supply the income and really a lot of the financial confidence that you’re going to experience or not experience as you go through retirement. That’s why it is pivotal for you to know your numbers and understand what those numbers actually mean to you. These numbers in retirement can be deceptive. Going back to that million dollar example, that’s all in a pre-tax IRA, which means part of that IRA is still owned by the IRS. Because when you take income from the IRA, that’s not all yours. You have to pay the IRS. Depending upon the state that you live in, you might have to pay your state as well. So that 4% income, where you’re taking 4% out of a million, that’s $40,000 of gross income, but it’s not spendable income.

Loren Merkle [00:23:03]:

So what you really want to focus on when you’re trying to plan for your lifestyle and how much your lifestyle is going to cost you, then where you’re going to deliver this income from is what do you actually get to spend in retirement? It’s not about what you make, it’s about what you get to keep what you get to spend. So we have to look at that net number, even after taxes.

Molly Nelson [00:23:25]:

So you’re telling me if I have a million dollars in an IRA, I don’t have a million dollars to spend, especially if I don’t do anything with the IRA. Let’s say I just spend right out of it. I don’t do Roth conversions, any of that stuff. It’s really only going to end up being a lot less than a million dollars.

Loren Merkle [00:23:37]:

One of the biggest surprises when we’re talking about this type of concept to families and individuals, individuals that we’re working with, you have a million dollars. Your retirement tax bill might be in excess of $500,000. Now that’s projecting over a 25 year time horizon over the course of retirement, and that does include growth on the million dollars. So it’s not like you only have $500,000 of the million to spend, but your retirement tax bill can be significant. The good news is, is that there’s steps that you can employ, strategies that you can employ to help decrease that retirement tax bill and increase your spendability.

Molly Nelson [00:24:15]:

And one more number that’s important is your lifestyle. And a lot of people for a long time when they’re getting close to retirement, haven’t had to think about a budget for a while. You know, they’re in the high wage earning years, they have more disposable income. But as you get a little closer to retirement, it’s a good idea to have at least an idea of about how much you might need to spend each month.

Loren Merkle [00:24:32]:

We need to have some kind of working number of what that’s going to look like. And sometimes people just can’t come up with it because they haven’t had to for the last 15 years. But we can work backwards within our planning. We can say, here’s all the different income sources, resources that you have. Here’s how much you can afford to spend on a monthly basis and still have a high probability of not running out of money before you run out of time. So that’s something that we do frequently because it can be a challenge and it’s not really a lot of fun to say, hey, let’s put some handcuffs around my lifestyle from a budgetary standpoint. But it is important because what you don’t want to do is start spending more than what you can afford and not not know it. And then seven years into retirement be like, whoops, now I really have to cut that back or your retirement financially is not going to last as long as you thought.

Molly Nelson [00:25:23]:

So not only is spending a mindset shift, investing is a mindset shift, and taxes are a mindset shift. It’s all a mindset shift. And there is a lot you have to rethink when it comes to retirement. I think this online workshop series that you and the retirement planners have put together is a really great resource for people.

Loren Merkle [00:25:37]:

Because it really digs deep into each one of those different pillars of a retirement plan. We’re talking about the lifestyle, how to create a lifestyle plan, how to create an income plan, tax plan, legacy plan, health care plan and investment plan. We have an online workshop dedicated to each one of those, and we go through specific strategies that you may be able to take out of that workshop implement almost immediately to help what you’re trying to accomplish from a retirement plan and standpoint. And the whole goal in mind is to give you confidence on these permanent decisions you’re going to have to make that you’ve never had to make before. So you’re not waking up five years into retirement and saying, whoops, I wish I would have known that. Or I wish I would have made that decision. You’re making these decisions when you have to make these decisions with confidence in knowing that you’ve done your due diligence the best that you can as you have to make these decisions.

Molly Nelson [00:26:33]:

I think that’s why the legacy planning workshop has been so popular, because you go over those three often overlooked legacy planning documents that people need to know about.

Loren Merkle [00:26:41]:

So much confusion. A lot of people have a will. Many people have an outdated will. Maybe they set it up 20 years ago when Junior was 17. Right? So you need to update some of those documents. But a lot of people think the will will take care of everything they’re trying to accomplish, when really there’s so much more that goes into a legacy plan. And it doesn’t mean it’s difficult. It doesn’t mean it needs to be complex.

Loren Merkle [00:27:04]:

It can be as simple as putting a beneficiary or multiple beneficiaries on your accounts. The thing is, is you have to know how to do it, what that should look like, and what ultimately it’s going to accomplish. To make sure that what your legacy ambitions are are really accomplished through these different documents.

Molly Nelson [00:27:22]:

You can watch that legacy planning workshop and more at RethinkRetirementSeries.com. This is Retiring Today and we thank you for watching.

Voice Over [00:27:35]:

Do I have enough saved for retirement? When should I take Social Security? Which Medicare option is best? How do I plan for inflation? Sometimes the road to retirement starts with more questions than answers. We’re here to help. Join us for our upcoming Journey to Retirement workshop. Get answers and start your retirement journey with confidence. Our online workshop includes information on Secure Act 2.0 and changing retirement rules. Visit RetireWithMerkle.com to register for an upcoming workshop. Your retirement journey starts now.

–––

We are an independent financial services firm helping individuals create retirement strategies using a variety of investment and insurance products to custom suit their needs and objectives. The content and examples shared are for informational purposes only and should not be construed as investment advice or serve as the sole basis for making financial decisions. Individuals are encouraged to consult with a qualified professional before making any decisions about their personal financial situation. Our firm is not permitted to offer legal advice. Investment Advisory Services offered through Elite Retirement Planning, LLC. Insurance Services offered through MRP Insurance, LLC.