Market volatility is unsettling, and it’s easy to make mistakes when emotions take over. Retirement Planners Chawn Honkomp and Loren Merkle tackle the most common investor missteps—and how to avoid them. From panic selling during downturns to sitting on the sidelines waiting for the “perfect time,” and even holding on to investments too long, they discuss why these habits can be so damaging. Most importantly, they share practical solutions like dollar cost averaging, diversification, and tax-smart strategies that can help keep your retirement on track no matter what the markets are doing.

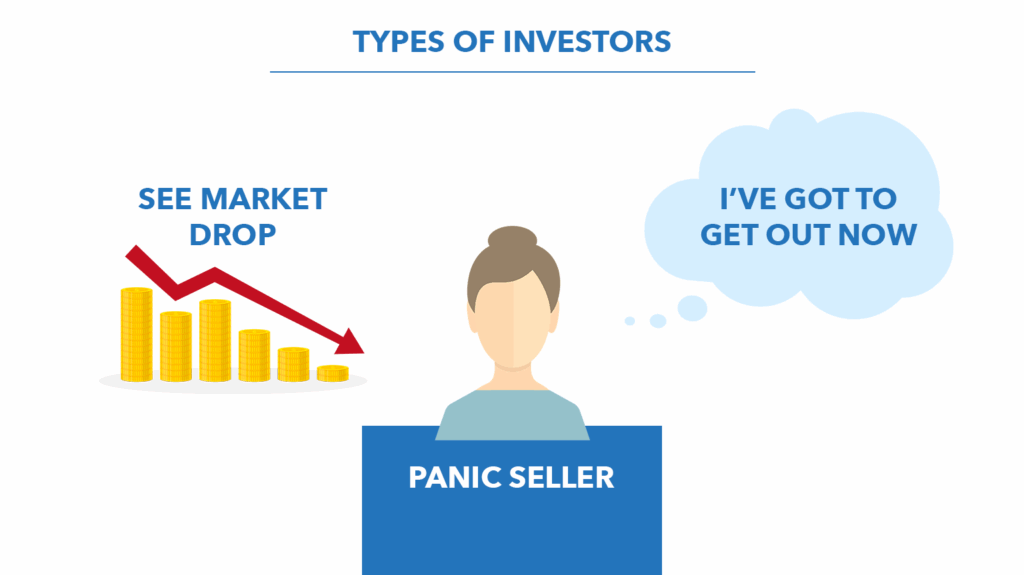

The Panic Seller

When markets tumble, panic sellers rush to the exits. They fear deeper losses and want to protect what they’ve saved. But as Chawn warned that instinct can backfire, referencing the steep declines in both the bond and stock markets in 2022.

“So many people were looking at what seemed like the writing on the wall and say, now’s the time, I gotta sell,” Chawn said.

The problem isn’t just when to sell, but also when to get back in—a choice that’s nearly impossible to get right. Loren noted what happened in recent years.

“For people that did take action in 2022…we saw the next two years of really strong market years,” Loren said.

History shows brighter days usually follow downturns. Loren notes that since the late 1930s, the S&P 500 has only been down three consecutive years twice. Adding that over the last two decades, it’s been up 80% of the time. That historical perspective, combined with knowing how much risk you’re actually taking, helps panic sellers avoid costly mistakes.

The Sideliner

Sideliners often sit in cash, waiting for the “perfect” moment to invest again. The trouble is that rebounds usually happen fast. Chawn recalled the COVID downturn.

“March of 2020, the S&P 500 lost 34% within a matter of weeks… and then the second half of 2020 the S&P 500 just skyrocketed,” he said.

Those who stayed in cash missed out on the recovery. A practical alternative is dollar-cost averaging (DCA). Loren explained how it works.

“Dollar-cost averaging… is a systematic approach of now taking that cash… and periodically investing that money back into the markets,” Loren said.

Loren adds that even retirees can use portfolio strategies that allow them to buy low during downturns while keeping a safe segment of money protected.

The Clinger

Clingers hold on to investments too long, sometimes out of loyalty, sometimes out of fear. Loren described a common example.

“Maybe sometimes it’s your employer… you own that stock. So no matter what it does, you feel like it’s going to work out,” Loren said.

But stubbornness can mean missed opportunities. Chawn highlighted tax-loss harvesting, a strategy for taxable accounts.

“You can sell that position… realize that loss… rebuy it after 31 days… and eventually it’ll come back up, you make money and you get a tax loss,” Chawn said.

Done carefully, this can turn short-term losses into long-term tax benefits.

The Lookie-Loo

Lookie-Loos watch the markets constantly, often feeling helpless when portfolios dip. Loren has seen it often.

“On a down day, you sit there and you ponder a little bit… the negative tends to sit with people a little bit more,” he said.

The key is putting proactive steps in place before downturns hit. One powerful example is Roth conversions.

“Once it gets into the Roth IRA, it grows tax free forever… (for some) it really makes sense to do a Roth conversion when the market’s down,” Chawn said.

With planning, market volatility becomes opportunity instead of fear.

Conclusion

If you see yourself in one of these investor types, that’s okay. These habits are common, especially when emotions run high during market swings. The good news is now you know the patterns—and with that awareness, you can make more intentional choices before the next market downturn.

Watch the full episode on YouTube to learn more about the 4 types of investors and the mistakes they can make in retirement.