A market downturn early in retirement can have a lasting impact on your financial future. This blog walks through a hypothetical example of the impact of market volatility and explores strategies to help protect your retirement income.

Why the First Year Matters More Than You Think

There’s never a “good” time for the market to drop—but the timing of a downturn can make a big difference.

For those nearing or entering retirement, that first year is especially critical. That’s because you’re no longer building your portfolio—you’re relying on it.

A $750,000 Portfolio Put to the Test

To understand the impact, Retirement Planner Chawn Honkomp walked through a hypothetical example.

A couple enters retirement with a $750,000 portfolio and plans to withdraw $3,500 per month, or $42,000 per year, to support their lifestyle.

At first, that may seem reasonable.

In year one, that withdrawal represents a 5.6% withdrawal rate.

What Happens When the Market Drops 30%?

Now imagine that same hypothetical couple experiences a 30% market drop in their first year of retirement.

Their $750,000 portfolio falls to $525,000.

Their lifestyle hasn’t changed—they still need $42,000 per year to live. But now, that same withdrawal is coming from a much smaller portfolio.

Chawn explains, “they’re taking the same amount of money out, but this is on a lower portfolio total.”

That pushes their withdrawal rate up to 8%.

The Impact of Market Swings

At first glance, going from 5.6% to 8% might not seem like a major change.

But over time, it can significantly increase the risk of running out of money.

As Chawn puts it, “a higher withdrawal rate on your total portfolio increases the likelihood of you running out of money.”

This is known as sequence of returns risk—when poor market performance early in retirement has the potential to significantly decrease your portfolio value.

The Real Risk: Selling in a Down Market

The issue isn’t just that the portfolio dropped—it’s what happens next.

When you’re retired, you don’t have the luxury of waiting for the market to recover before taking income.

As Chawn explains, “when you’re in the spending stage of life… those market drops can have a bigger impact on your overall plan.”

You may be forced to sell investments while they’re down, locking in losses and leaving less behind to recover.

You Can’t Predict the Market—but You Can Prepare

Everyone wants to know when the next downturn will happen.

The reality is, no one knows for sure.

As Retirement Planner Loren Merkle says, “we know we’re going to continue to have market drops, but what we don’t know is when that drop will happen.”

That uncertainty is exactly why planning is so important.

Building a Strategy That Can Withstand a Downturn

The key isn’t avoiding market drops—it’s structuring your plan in a way that can help keep a downturn from having a larger impact on your retirement.

One approach is separating your money based on when you’ll need it.

Loren describes this as being more intentional: “you have to be more intentional at this phase of your life.”

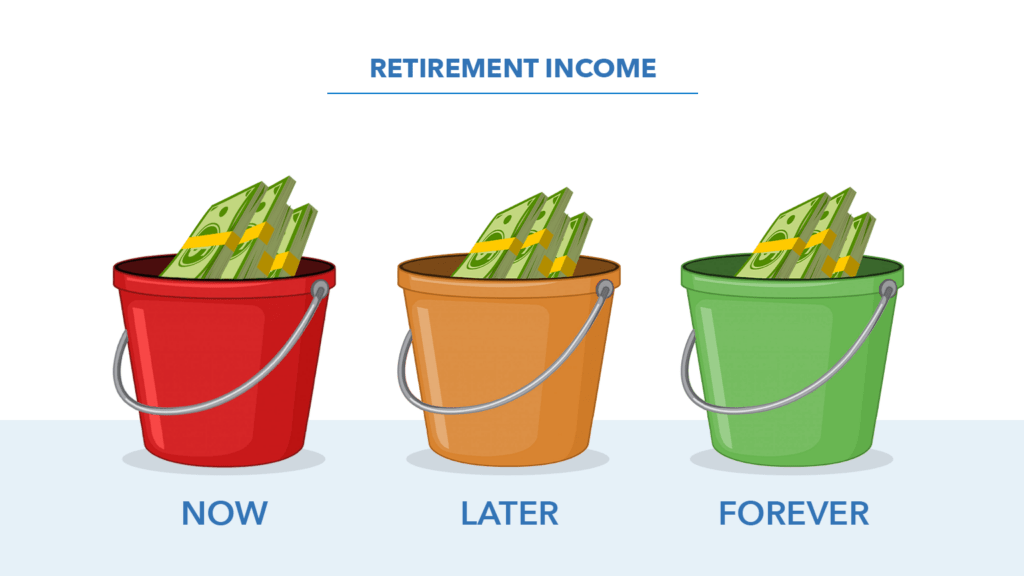

A structured approach—like a bucket strategy—can help:

- A short-term income bucket for current expenses

- A mid-term bucket for future withdrawals

- A long-term bucket for growth

This may help you continue taking income without needing to sell investments at a loss.

As Chawn explains, having that short-term bucket means “you can count on the money that’s in the now bucket because that’s what you’re going to take out for income.”

The Bottom Line

A market drop in your first year of retirement isn’t just stressful—it can potentially change the trajectory of your entire plan.

The difference between a 5.6% withdrawal rate and an 8% withdrawal rate may come down to timing—but the consequences can last for decades.

That’s why retirement planning isn’t just about growing your money—it’s about protecting it when it matters most.

Or as Loren puts it, “you have to be more intentional at this phase of your life.”

For many, one way to help prepare for market swings is to adjust their investment strategy as they get closer to retirement.

Watch the full episode on YouTube and learn more about the impact of market volatility and explore strategies to help protect your retirement income.