Many people assume their retirement savings tell them everything they need to know about the future. This article explores why a 401(k) is only one piece of the puzzle and what a true written retirement plan includes, from income and taxes to health care and legacy planning.

The 401(k) Balance

For many people approaching retirement, the quarterly 401(k) statement feels reassuring. The balance is there. The performance is tracked. It looks like a plan.

But as Retirement Planner Chawn Honkomp explains, that sense of security can be misleading. He notes that people look at their statements and think, “all right, here’s my plan,” because they can see balances and performance, but “there’s much more to your stage of life as you get closer and closer to retirement.”

A 401(k) shows how much you’ve saved. It doesn’t show how retirement actually works.

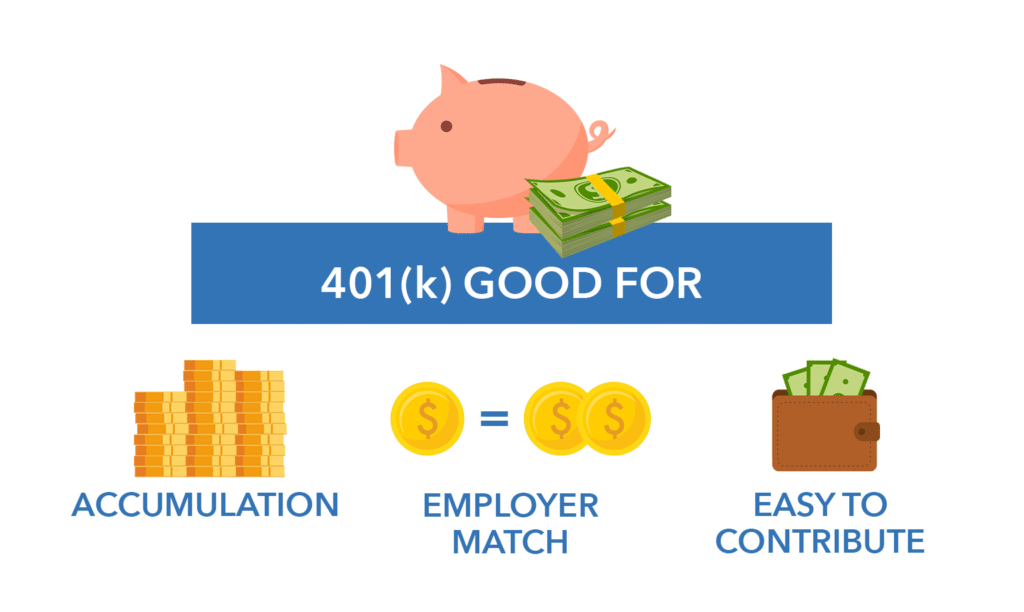

What a 401(k) Is Good For

A 401(k) plays an important role, just not the one many people assume. Retirement Planner Loren Merkle describes it as “really good for enabling you to enter a phase of your life where you can live and have fun and not have to work,” because it allows you to accumulate money consistently over time.

Loren points out that the real advantage is time. Contributing each pay period and letting those dollars grow, whether pre-tax or after tax, builds the foundation for retirement. As he puts it, “time is by far your biggest weapon.”

That foundation matters. But accumulation alone doesn’t answer retirement’s biggest questions.

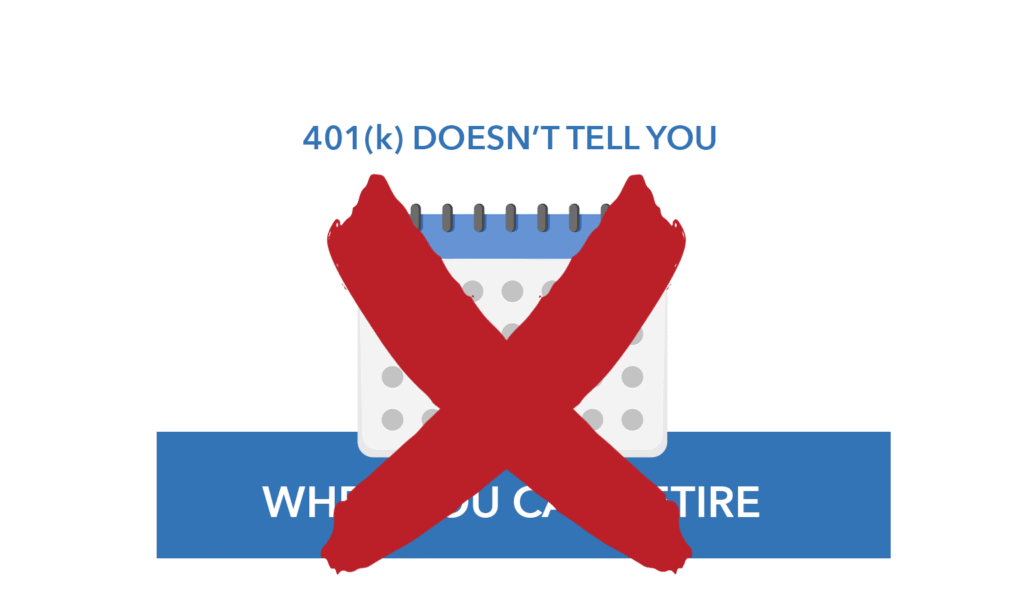

The Questions a 401(k) Cannot Answer

As retirement gets closer, people start asking questions about their account that statements likely won’t answer.

A 401(k) doesn’t outline when you can retire. It doesn’t tell you how much you can safely spend each month. It doesn’t include details about a retirement income plan that includes your other sources of income, like Social Security, and how those sources will be taxed.

Chawn emphasizes that investment balances are just one piece, adding that a written retirement plan includes multiple components because when you are getting ready to retire “everybody knows they’ve got to start thinking about more.”

Thinking Ahead

Loren says that sometimes people don’t recognize how complex retirement is until they are “on the doorsteps of retiring.” Suddenly, decisions appear that they’ve never had to make before, including how to take money out of their 401(k).

Loren highlights a rule that can catch some off guard: “(In many cases) when you take money out of your 401(k) plan, there is a mandatory federal tax withholding of 20%.”

Add in early withdrawal rules, tax penalties, and income timing, and the simplicity of saving turns into a maze of decisions.

What a Written Retirement Plan Really Is

A written retirement plan can help bring clarity to retirement decisions. The plans that Loren and Chawn help families and individuals create are called a RetireSecure Roadmap, built around six pillars: lifestyle, income, taxes, investments, health care, and legacy.

Loren explains that the RetireSecure Roadmap helps people “make the decisions that they have to make.” Instead of guessing, families can see how their retirement decisions work together.

Starting With Lifestyle

The foundation of the plan is lifestyle. Loren says this pillar answers a simple but powerful question: “What are you going to do in retirement?”

Travel, time with grandkids, seasonal living — all of it gets written down. Loren explains that the lifestyle plan matters because “that’s going to determine how much your retirement is going to cost you,” and every other pillar supports that vision.

Turning Lifestyle Into Income

Once lifestyle goals are clear, the income plan shows how to fund them. Chawn describes starting with the basics: “What a typical month is going to look like for you,” including expenses that don’t happen every month.

From there, income sources are coordinated — Social Security, pensions, and portfolio withdrawals. Chawn notes that the goal is to “take the right distributions from the right accounts at the best time.”

Loren adds that answering whether you can fund your lifestyle before retirement provides clarity. “You’re going to come up with one of two answers,” he says. Either you have enough, or you don’t — and knowing sooner gives you time to adjust.

Planning for Taxes Before They Surprise You

Taxes don’t disappear in retirement, and Loren says nearly everyone will face a retirement tax bill. The question is “how big is that retirement tax bill going to be?”

A written plan can show the long-term impact of retirement income and outlines strategies — year by year — that can potentially reduce that burden. Chawn emphasizes control, noting that without planning, people simply pay taxes on the IRS schedule instead of being intentional.

Investing With Income in Mind

Retirement investing is different. Loren explains that market drops feel very different when your lifestyle depends on withdrawals. “If your portfolio drops by 30%,” he says, “your lifestyle could also drop by 30%.” Loren says that building a portfolio designed with income in mind can help provide stability through different market conditions, helping retirees avoid running out of money before they run out of time.

Addressing health care and Legacy

Health care is often one of the biggest concerns. Loren explains that plans must reflect whether someone is pre-Medicare or post-Medicare and adapt as options and costs change over time.

The legacy pillar brings everything full circle. Chawn explains it’s about making sure assets transfer efficiently to the people or causes that matter most, with beneficiary designations and legal documents aligned with the overall plan.

Clarity Changes Everything

At the heart of a written retirement plan is clarity. Seeing everything in one place can help people answer the question they worry about most: Do I have enough?

As Chawn puts it, once people see the full picture, they move from worrying about money to understanding it — and that shift can make all the difference.

Watch the full episode on YouTube and learn more about written retirement plans.