A large IRA can be a powerful retirement asset—but it also comes with tax implications and planning decisions. This blog explores three strategies retirement planners often consider for large IRAs: reducing taxes strategically, turning savings into reliable retirement income, and creating a lasting legacy.

Understanding the Basics of an IRA

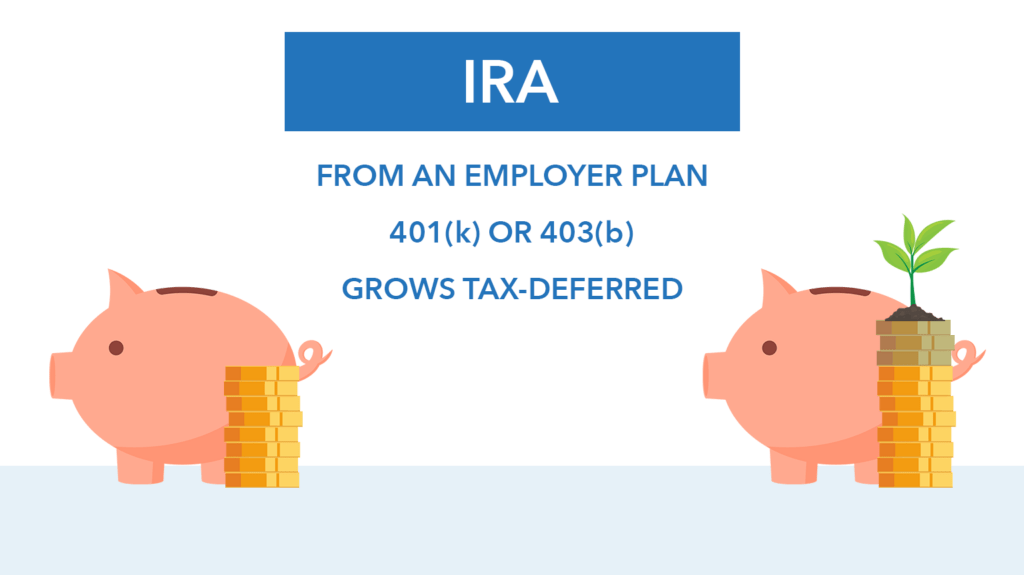

An IRA or Individual Retirement Account is one of the most common ways Americans save for retirement. These accounts are often funded in two primary ways: direct contributions or rollovers from workplace retirement plans like a 401(k) or 403(b).

When someone contributes to a traditional IRA and qualifies for the deduction, the contribution can reduce taxable income in the year it’s made. The money inside the account then grows tax deferred until it’s withdrawn later in life.

Another common path into an IRA happens when someone leaves an employer and rolls over their workplace retirement plan into an IRA. Retirement Planner Loren Merkle explains that those dollars continue growing tax deferred until distributions begin.

Beyond tax deferral, IRAs often offer more flexibility than employer plans. Many workplace plans limit participants to a short list of investment options. With an IRA, investors typically gain access to a much broader range of investments.

That flexibility can also make consolidation appealing. Over the course of a long career, it’s not unusual for someone to accumulate multiple old retirement plans from previous employers. Rolling those accounts into a single IRA can make them easier to track and integrate into a broader retirement strategy.

Strategy 1: Converting to a Roth IRA

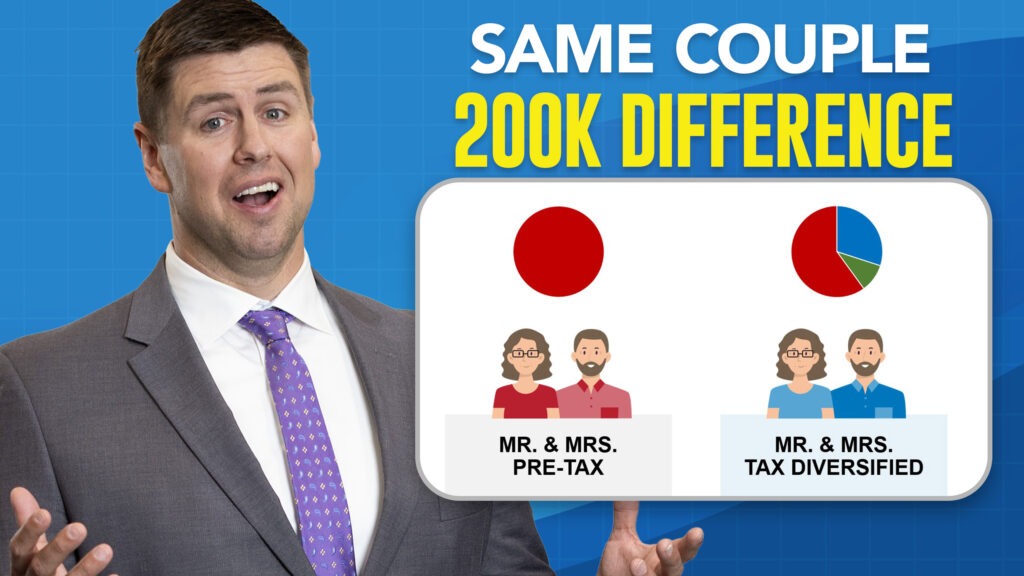

As IRA balances grow, taxes become an increasingly important planning consideration. Every dollar withdrawn from a traditional IRA is generally taxable as income.

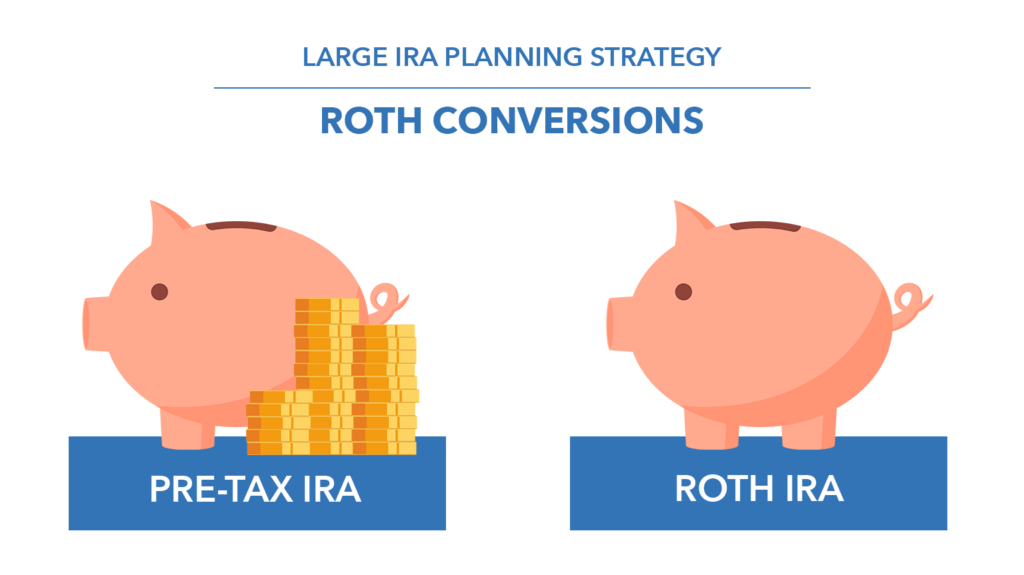

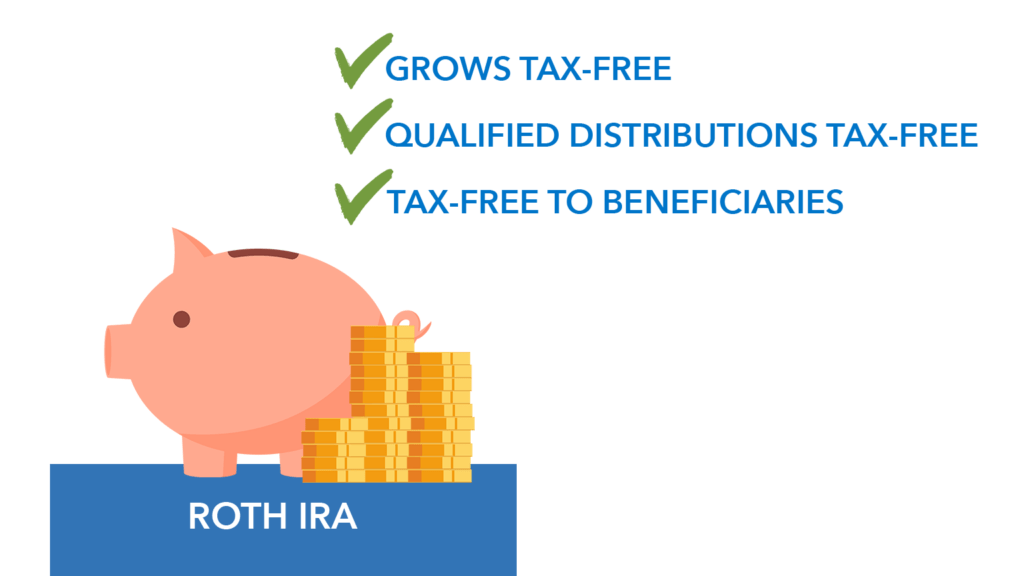

One strategy to explore is converting part of a traditional IRA to a Roth IRA. The conversion requires paying taxes on the amount moved in the year the conversion occurs, but qualified distributions from the Roth can be tax free.

Loren summarizes the appeal this way: “The only thing better than a large IRA is a large tax-free IRA.”

But Roth conversions require careful timing. Moving too much money in a single year could push someone into a higher tax bracket and reduce the benefit of the strategy.

Loren emphasizes that the goal is to manage taxes strategically over time. “You want to make sure that you’re actually doing what you set out to do, which is decrease your retirement tax bill instead of increasing it.”

For some retirees, the best window for conversions occurs after leaving the workforce but before required minimum distributions begin. During this period, taxable income may temporarily fall, creating opportunities to convert portions of an IRA at lower tax rates.

Strategy 2: Turning an IRA into Retirement Income

A large IRA may look reassuring on paper, but many pre-retirees struggle with the next question: how do you actually turn that balance into income?

Retirement Planner Clint Huntrods says the process begins by building a comprehensive retirement plan rather than focusing solely on investments.

“As we think about helping families, we really want to start by building that comprehensive retirement plan first,” Huntrods says. “That will start to drive the investment decisions that are appropriate for any individual family.”

Clint shared a hypothetical example about a couple with $2 million in IRA savings. The hypothetical couple’s goal was to maintain a lifestyle requiring about $10,000 per month.

Social Security benefits were expected to provide about $5,500 per month. That left a gap of roughly $4,500 each month that needed to come from their savings.

Instead of simply withdrawing from the IRA as needed, Clint showed a strategy where the couple divided the portfolio so each portion had a different purpose.

A portion was set aside for an income strategy designed to produce roughly $4,500 per month, matching the couple’s income gap. Other portions of the portfolio were allocated for shorter-term needs and longer-term growth.

Clint concluded by adding how a strategy like this can give those approaching retirement confidence because their retirement savings had a purpose within an overall retirement plan. Some assets provide stability and income, while others remain invested for possible growth.

Strategy 3: Creating a Charitable Legacy

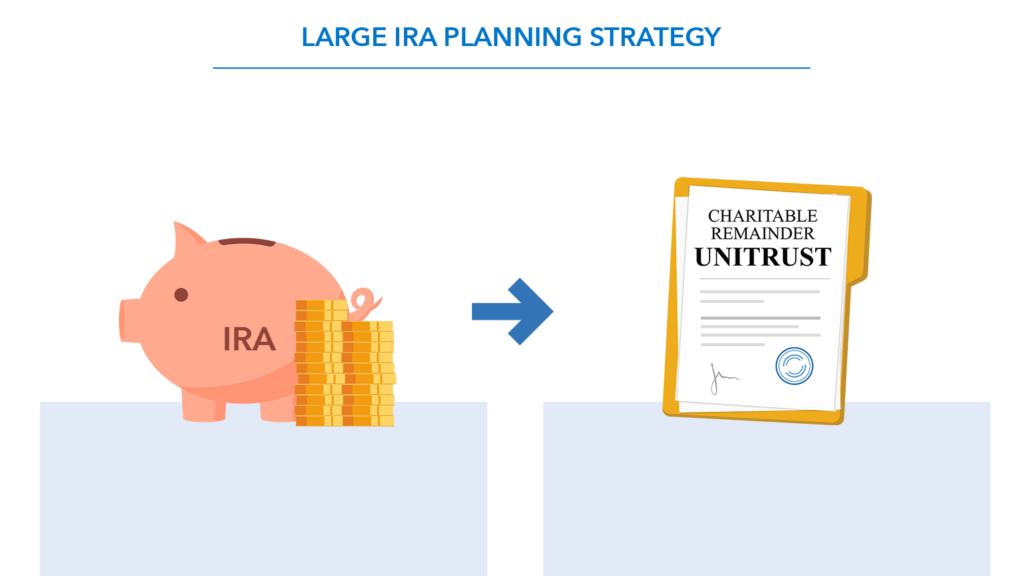

For retirees who are charitably inclined, an IRA can also play a role in legacy planning.

One advanced strategy involves naming a charitable remainder unitrust as the beneficiary of an IRA. In this arrangement, the IRA assets transfer into a trust at death. The trust then distributes income to beneficiaries—often children—for a set period of time or for life.

Loren explains how the concept works in practice. “The trust would pay out their beneficiaries over a designated period of time or for their life.”

In one hypothetical example, a couple with a $2 million IRA might structure the trust to pay about 5 percent annually to their beneficiaries for 20 years. Over time, that could provide significant income to the family.

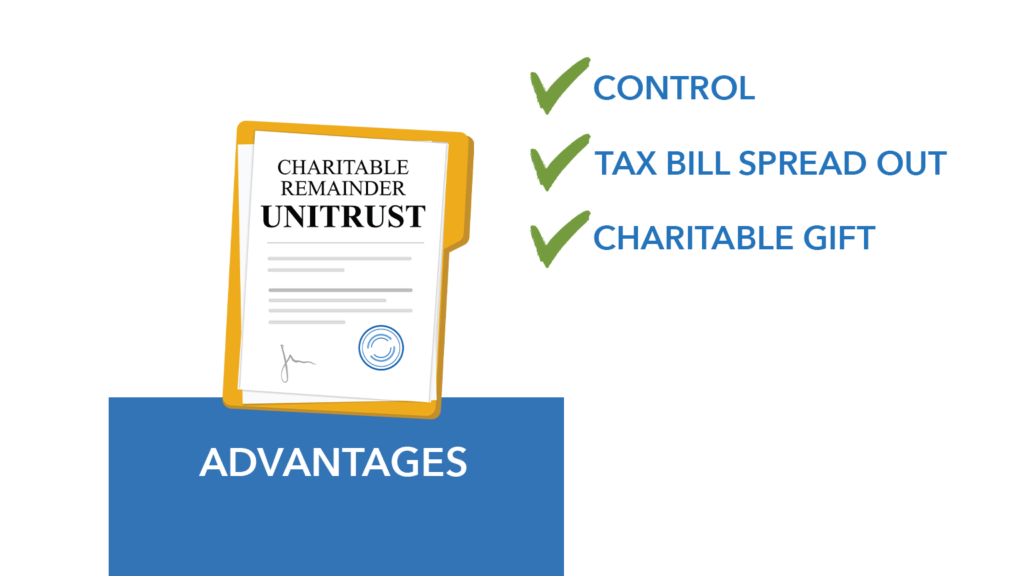

When the payout period ends, any remaining assets in the trust are distributed to the designated charity.

Loren notes that several potential advantages come with this type of strategy. “You can have a controlled payout to your kids, so they don’t just receive the full amount all at once.”

The approach can also spread the tax burden over a longer period while fulfilling charitable goals. However, it is a complex strategy that requires coordination with estate planning attorneys and tax professionals.

Planning Matters More as IRA Balances Grow

A large IRA represents years—sometimes decades—of disciplined saving. But as retirement approaches, the focus often shifts from accumulation to strategy.

Tax planning, income generation, and legacy goals all intersect with how IRA assets are used. And as balances grow larger, those decisions can have an even greater impact on long-term outcomes.

With thoughtful planning, an IRA can do more than fund retirement. It can provide steady income, reduce tax exposure, and even support the causes and people retirees care about most.

Watch the full episode on YouTube and learn more about strategies to reduce your tax bill.