When it comes to Medicare, misinformation travels fast. Maybe a friend insists it’s free. A coworker swears long-term care is covered. Someone else warns you about penalties for signing up too late. The truth? Some of what you hear is right—but a lot of it isn’t.

You’ll learn what Medicare actually covers, what it costs, how to avoid penalties, and the choices you’ll have when it’s your turn to enroll. Retirement Planner Loren Merkle and Director of Medicare & Long-Term Care AnnaMarie Morrow will help you separate Medicare fact from fiction and to help build a plan that supports your full retirement picture.

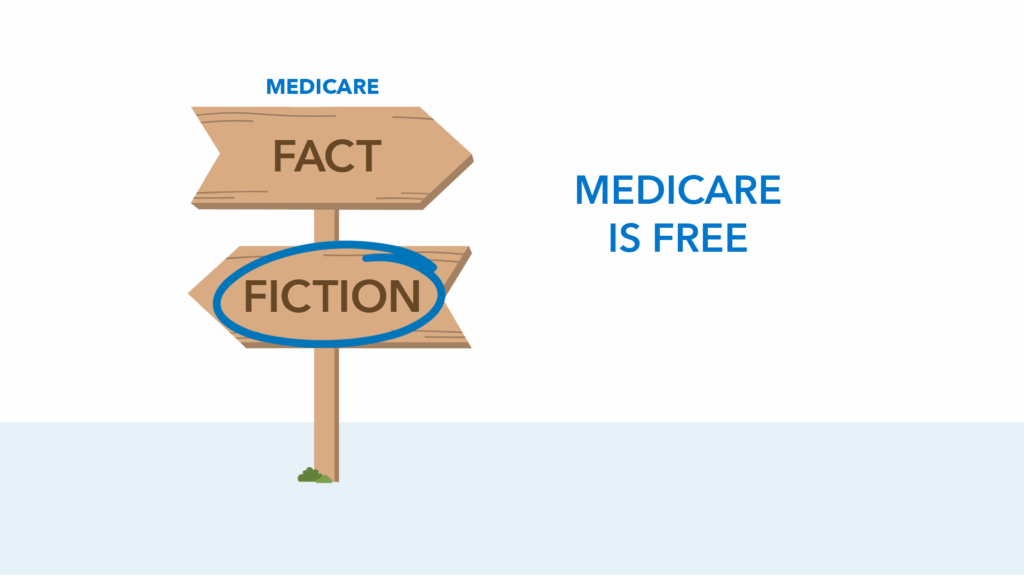

1. “Medicare is free.”

Fiction.

AnnaMarie says this is one of the most common misconceptions. “There is this misconception where Medicare is free,” she explains, “but then when we break it down, part A is hospital insurance, and as long as you or your spouse have worked the qualified number of quarters, then you’ve already paid for part A while paying your taxes. So there is no monthly premium for part A, but Medicare Part B… there is a monthly premium for that which is also based on your income.”

Loren adds that understanding those costs ahead of time is essential. “Your health care costs can make up a good part of that monthly budget,” he says. “Many people think Medicare will cost you less than what your group plan cost you—and in some cases it will—but in many cases, Medicare can actually cost you more.”

2. “Medicare covers long-term care.”

Fiction.

People often assume Medicare will pay for an extended nursing home stay or assisted living, but that’s not the case. AnnaMarie notes that while “you may see inpatient hospital stay or skilled nursing stay 90 days,” that coverage is temporary. “That is not a long time,” she says. “What happens after just three months? Medicare stops covering. And that is when you would need to have a plan in place for long-term care costs.”

Loren puts the numbers in perspective: “The average need for long-term care for a female is somewhere around 3.2 years and for a male is 2.2. So that three months is just not going to cover the average need for most people in the United States.”

He adds that talking about long-term care is difficult but critical. “It is so expensive; most people don’t want to talk about it,” Loren says. He adds that building a plan for long-term care, if you need it, into a retirement plan can help manage the risk of unexpected expenses in retirement.

3. “You can be penalized for signing up late for Medicare.”

Fact.

Late enrollment penalties are real, but they’re avoidable if you understand the rules. “It is vital to make sure that your employer coverage is considered qualified group employer coverage,” AnnaMarie says. “If you are on COBRA, it is not considered qualified.”

Loren adds that the warning letters people receive can be intimidating. “It’s almost like a big, flashy neon sign in the mail just blinking ‘You’re going to have penalties!’” He adds, “but it’s not that bad. You just need to be alerted—this is a decision point.”

4. “Medicare covers all your health care needs.”

Fiction.

AnnaMarie is clear: “Dental, hearing aids, anything elective based on their patients, these are not covered.” Some supplemental plans can help with those “ancillary benefits,” but Medicare itself leaves gaps.

Loren reminds people not to assume it’s comprehensive. “We would like it to cover all of our health care needs,” he says, “but the facts are it doesn’t.”

5. “You have choices with Medicare.”

Fact.

“You have A and B offered by the government,” AnnaMarie explains, “but then your options are supplemental plans. Parts A and B were not created to be a retiree’s sole form of health insurance.” She points out that’s why private carriers offer Medigap and Advantage plans—to “fill in the gaps that exist within A and B.”

Loren adds that the choices don’t end once you sign up. “It’s something that needs to be reevaluated and reevaluated each and every year,” he says. “If you take advantage of the options that you have, you can really create a plan that works well for you.”

AnnaMarie agrees, saying one-on-one conversations make it much easier to cut through confusion. “When people research Medicare on their own, that’s when anxiety sets in,” she says. “But after 15 or 20 minutes in a one-on-one conversation, my favorite thing to hear is, ‘Well, that was easy.’”

6. “You can change Medicare plans each year.”

Fact.

Annual open enrollment runs from October 15th to December 7th, and even if your prescriptions haven’t changed, your coverage might have. “These drug cards, they can and typically do change,” AnnaMarie says. “Pharmacies can opt in whether they’re preferred in network, standard in network or out of network. That can also change.”

She’s seen dramatic differences. “We’ve seen [a copay] go from $15 for a 90-day supply to over $500.” Loren calls that kind of surprise “a devastating price increase” that could potentially be avoided with annual check-ins.

7. “Medicare will notify me when it’s time to sign up.”

Fact and Fiction

“If you’re already receiving a Social Security benefit before you turn age 65, you’ll automatically be enrolled in Medicare A and B,” AnnaMarie says. “But if you have not elected your Social Security benefit, you’re getting all the mail.” She adds that while those letters about penalties do serve as a kind of notification, it’s not always clear to everyone that this is their cue to sign up.

Loren encourages proactive planning. “Have that conversation with a professional who understands Medicare,” he says. “Having that conversation with your friends or coworkers… that’s fun, but their life doesn’t necessarily mimic your life.”

8. “You have to enroll in Medicare at 65 even if you’re still working.”

Fiction.

AnnaMarie explains, “If you’re still working, and you’re on an employer group coverage plan or your spouse’s, just make sure it’s considered qualified by Medicare standards. You do not have to elect A and B when you turn age 65.”

But there are details to watch. “If you are making HSA contributions,” she says, “when you go to elect part A, you would need to shut off those contributions.” Loren adds that a personalized conversation helps “eliminate a lot of those nuances that are not particular to your situation.”

How Medicare Fits Into Your Overall Retirement Plan

AnnaMarie reminds people that Medicare doesn’t exist in a vacuum. “The costs we pay in Medicare are dependent on the income plan, the investment, the tax plan,” she says. “All of these pillars within the RetireSecure Roadmap can affect what you pay.”

Loren outlines the six pillars of the customized retirement plans we help families build: “You need an income plan, you need a tax plan, need an investment plan, you need a health care plan, and you also need a legacy plan.”

Medicare doesn’t have to be confusing, having the right information and support can help make it a more confident part of your retirement plan. As Loren says, the goal is to “eliminate the noise” and focus on “what you need to talk about.” And when that happens, AnnaMarie’s favorite line from the families and individuals she’s helped through the process rings true: “Well, that was easy.”

Watch the full episode on YouTube and learn more about Medicare.

Sources: LongTermCare.gov