Social Security can be one of the biggest financial decisions in retirement. This article explores when to claim, how different strategies impact your income, and why your decision should be part of a broader retirement plan.

The “Elephant in the Room” of Retirement

When it comes to retirement planning, few decisions carry as much weight—or confusion—as Social Security. It’s often discussed, frequently debated, and rarely fully understood.

As Retirement Planner Loren Merkle explains, Social Security “can be your largest guaranteed source of income in retirement, and that’s why when you file is so important.”

For many retirees, this benefit functions much like a pension—steady, predictable income that lasts for life. And the numbers are significant. Over a 20-year retirement, Loren says benefits may add up to $500,000 for an individual or over $1 million for a married couple, illustrating why Loren says the decision deserves careful thought.

Understanding Your Claiming Options

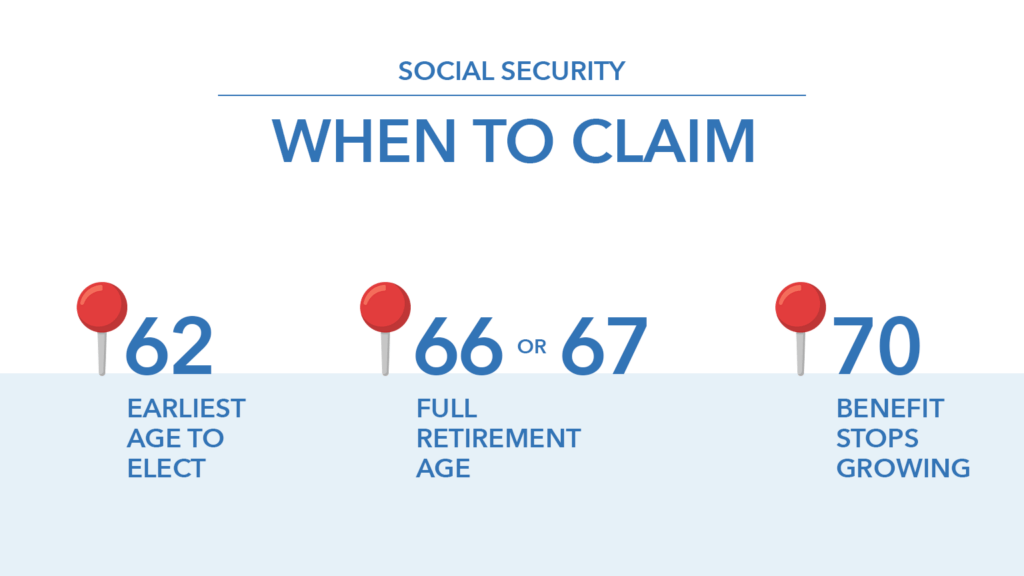

Most people focus on three key ages when claiming Social Security:

- Age 62 (earliest eligibility for most people)

- Full Retirement Age (FRA) (typically 66–67)

- Age 70 (maximum benefit)

The difference between these choices can be substantial.

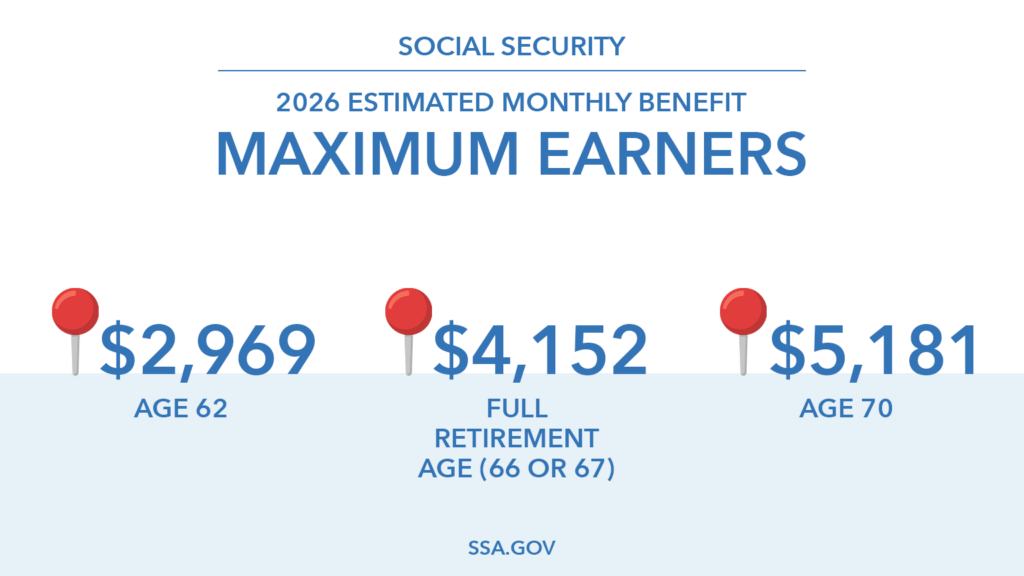

According to the Social Security Administration, the 2026 estimated monthly benefit for maximum earners is:

- Age 62: $2,969

- Full Retirement Age: $4,152

- Age 70: $5,181

The average estimated monthly benefit for all retirees is $2,071.

That’s why timing matters—and it can play an important role in your retirement plan.

Why It’s Important to Avoid One-Size-Fits-All Advice

One retirement planning pitfall can be relying on what others are doing.

Your Social Security decision should reflect:

- Your health and life expectancy

- Your income needs

- Your savings and investments

- Your retirement lifestyle

For example, someone with strong savings and good health may benefit from delaying. Someone with fewer assets or health concerns may need income sooner.

The key is personalization—not comparison.

A Redo is Difficult

Social Security isn’t something you can easily redo.

As Loren explains, “after 12 months… this becomes a permanent decision.”

While it is technically possible to reverse your choice early on, Retirement Planner Clint Huntrods cautions that “the government’s going to require that you repay what they paid you all at once.”

This is why thoughtful planning upfront is important.

Don’t Make the Decision in a Vacuum

A common mistake is treating Social Security as a standalone choice. In reality, it’s deeply connected to the rest of your financial plan.

Instead, your strategy should align with:

- Your income plan

- Your tax strategy

- Your investment allocation

- Your health care plan

When these pieces work together, your decision becomes clearer.

How Income Needs Shape the Strategy

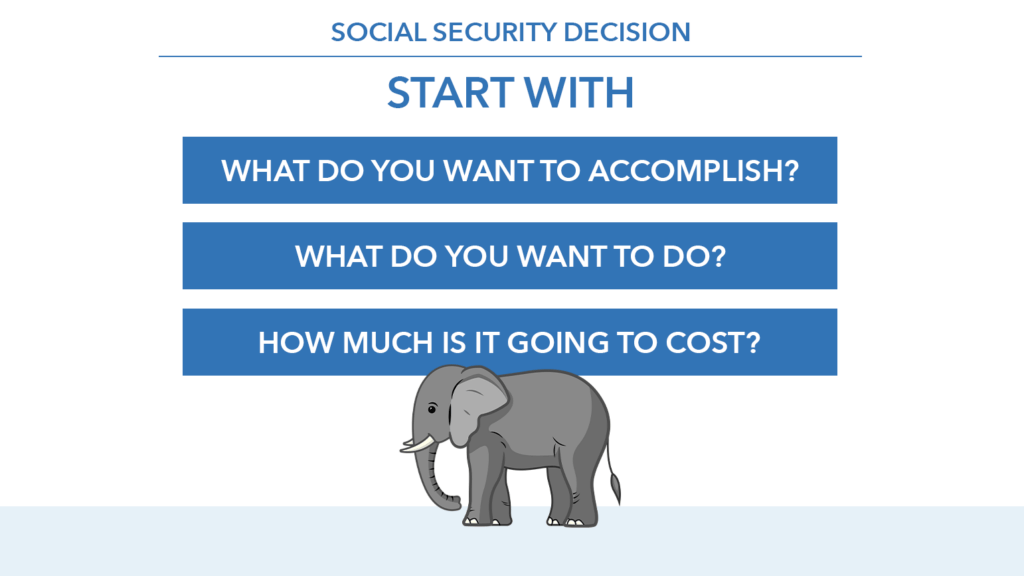

At its core, the Social Security decision often comes down to one simple question: Do you need the income now, or later?

Loren explains the framework: “What are you trying to accomplish in retirement? What is your lifestyle? How much is retirement going to cost you on a monthly basis?”

From there, you evaluate:

- What Social Security provides

- What your investments can support

- Whether delaying creates a better long-term outcome

In some cases, using investment income early may allow you to delay claiming, which can increase your future Social Security benefit. In others, claiming sooner may help preserve assets in some situations.

Flexibility Matters More Than Perfection

Even with a solid plan, life changes—and your strategy should adapt.

Loren highlights this flexibility: “the plan has to be flexible because life changes… your goals, your ambitions change, and circumstances can change.”

Markets shift. Health evolves. Priorities adjust.

A good plan isn’t rigid—it’s responsive.

Social Security is too important to leave to guesswork, opinions, or quick decisions.

It’s a major income source, a long-term commitment, and a key piece of your overall retirement strategy.

And when you approach it that way, the “elephant in the room” can become a lot more manageable.

Watch the full episode on YouTube and learn more about how different strategies impact your income, and why your decision should be part of a broader retirement plan.

Source: SSA.gov