A look at the massive wealth transfer underway, why families struggle to talk about inheritance, and how thoughtful planning can protect both wealth and relationships.

The Largest Wealth Transfer in History

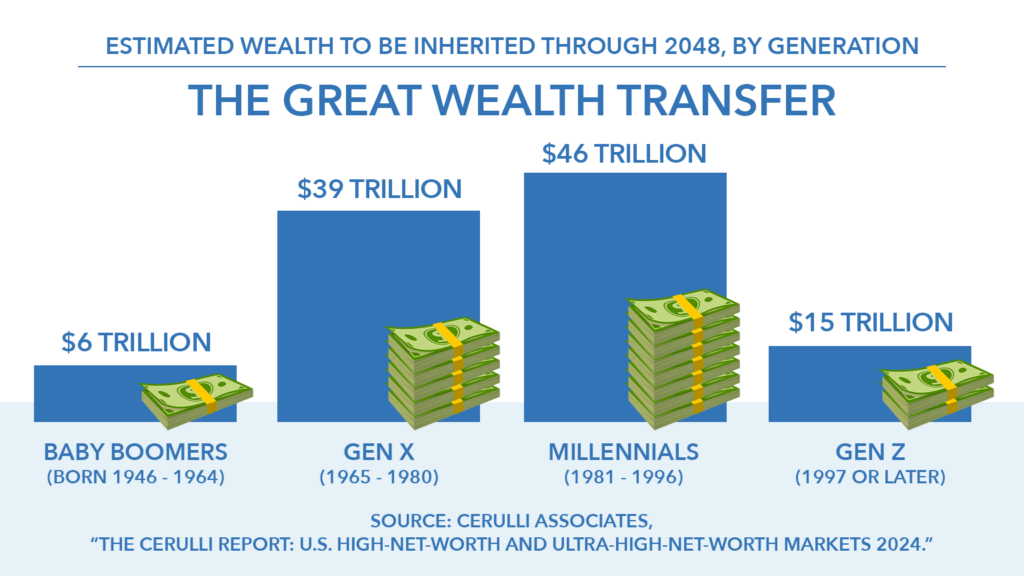

$124 trillion is expected to change hands over the next 20 years, according to estimates by the consulting firm Cerulli Associates.

Much of that wealth is currently held by baby boomers, and over the coming decades, it will largely flow to younger generations. Millennials alone are projected to receive about $46 trillion, followed by Gen X and Gen Z.

This shift isn’t just about money—it’s about preparation. Families are facing decisions not only about how to pass wealth on, but how to talk about it in the first place.

Why Families Aren’t Talking About It

Despite the scale of what’s coming, most families aren’t having open conversations about inheritance.

Retirement Planner Clint Huntrods explains, “It can be uncomfortable. It’s something that, you know, just isn’t always spoken of openly.”

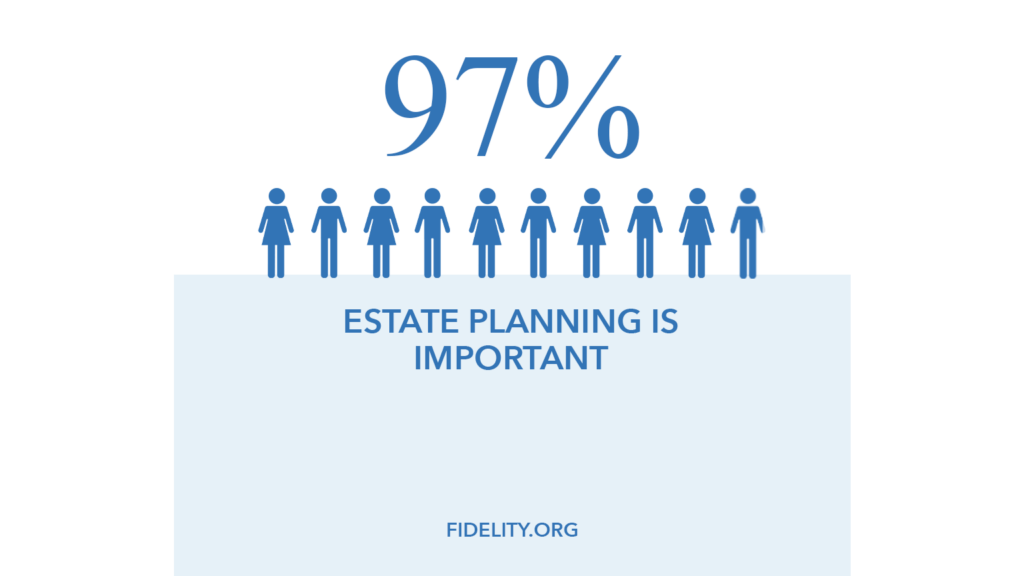

And yet, nearly everyone agrees these conversations matter. According to the Fidelity 2025 Family and Finance study, 97% of families say estate planning discussions are important—but 68% haven’t shared inheritance details with their children.

Retirement Planner Loren Merkle puts it simply: “Talking about money’s hard.”

There are generational differences at play, too. Loren notes that many baby boomers are more open to discussing finances, while their parents often avoided the topic altogether, creating a communication gap that still exists today.

The Cost of Silence

When families avoid these discussions, the consequences can go beyond finances.

Clint emphasizes the importance of clarity: “If there’s a void, if there’s a space where someone isn’t clearly communicating, oftentimes negativity can fill that.”

Without clear direction, beneficiaries may be left wondering why decisions were made or what to expect. That uncertainty can lead to confusion, conflict, and even strained relationships.

At the same time, many parents hesitate to share details for valid reasons. They may worry about creating dependency or setting expectations that could change over time. As Loren explains, “A lot of things can happen… you don’t really know how much money is going to be left in a lot of cases.”

Are Kids Ready for an Inheritance?

There’s also a disconnect between how prepared children feel and how prepared parents believe they are.

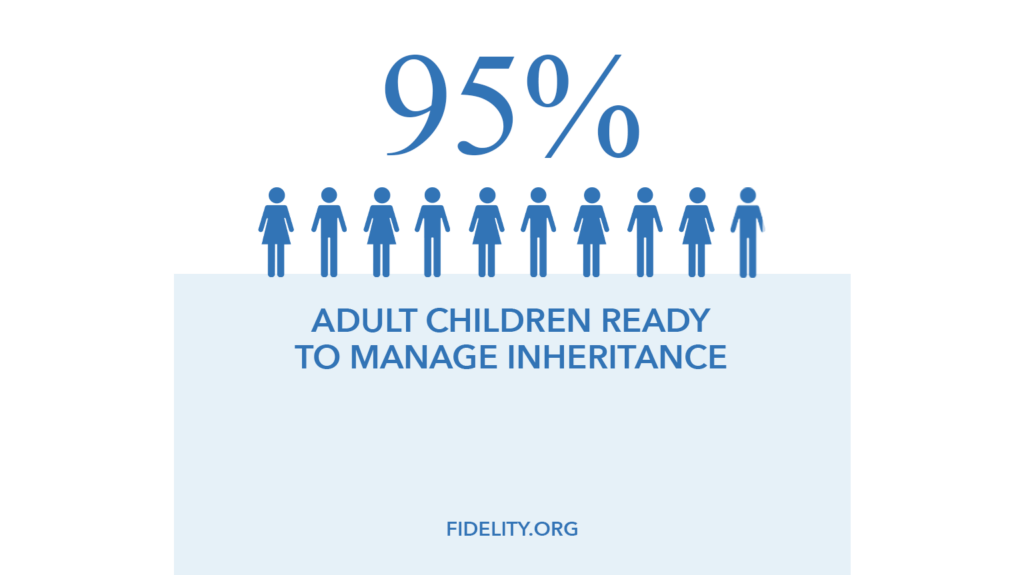

While 95% of adult children say they’re ready to manage inherited wealth, 25% of parents disagree, according to the Fidelity study.

That gap highlights a deeper issue—inheritance isn’t just a financial event, it’s a behavioral one. Without preparation, even well-intentioned plans can fall short.

A Hypothetical Example: The Hidden Tax Impact

Consider a hypothetical couple—Joe and Jane—who believed they were on track. After building out their plan, they discovered they were likely to leave about $2 million in pre-tax retirement accounts to their children.

Because the money is pre-tax, their children would have to withdraw it within 10 years and pay taxes at their own (higher) income levels. In this hypothetical example, both children were in roughly the 30% tax bracket.

That meant each child could face a significant annual tax burden—potentially pushing their effective tax rate as high as 45% when factoring in federal and state taxes.

The result? A projected tax bill of around $570,000 per child, or $1.14 million total on the $2 million inheritance.

Planning Can Create Opportunities

What if Joe and Jane did some proactive tax planning?

By strategically converting portions of their pre-tax savings into Roth accounts while they were in a lower tax bracket—they could reduce the future tax burden on their children.

Clint says the outcome could be significant: about $225,000 in tax savings per child, or $450,000 total.

Clint describes the shift: “They actually know there’s opportunities… to pay some tax on our tax bill rather than have that go to our kids where they’re going to be in a much higher tax range.”

Opening the Door to Conversations

For some families, involving children in the planning process can lead to meaningful outcomes.

In one case, a daughter reviewing her mother’s plan encouraged her to enjoy retirement more fully. Instead of preserving every dollar for inheritance, the focus shifted toward experiences—travel, time together, and living well now.

These conversations don’t have to reveal every detail. As Loren notes, “That can look like anything you want it to look like… whatever you’re comfortable with.”

What matters most is having a plan—and ensuring it’s understood, whether during your lifetime or after.

Planning Can Create Clarity

The $124 trillion wealth transfer is already underway. The question isn’t whether it will happen—it’s whether families will be prepared for it.

Planning can create clarity. Communication can build understanding. And together, they can help families move forward with intention—supporting both financial decisions and the relationships that matter most.

Watch the full episode on YouTube and learn more about how thoughtful planning can protect both wealth and relationships.

Source: Cerulli.com, Fidelity.com

This is a hypothetical example used for illustrative purposes only. It is not representative of any specific investment or combination of investments. There is no assurance or certainty that any investment or strategy will be successful in meeting objectives