Retirement planners Loren Merkle and Chawn Honkomp provide insight and action strategies that may help you sidestep common retirement income pitfalls. Let’s break down each trap and see how to safeguard your retirement.

–––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Trap #1: Not Spending Enough in Retirement

While many retirees worry about running out of money, a less obvious but equally damaging trap is not spending enough. This issue often affects diligent savers who struggle to shift from the accumulation mindset to the distribution phase of retirement.

The transition into retirement introduces a new set of questions—ones that people have never had to answer before. Despite having more freedom and time, many retirees are burdened with uncertainty about whether they can afford the lifestyle they desire. The fear of outliving their money can hold them back from fully enjoying what should be some of the most fulfilling years of their lives.

Loren highlights a key consequence of this trap: retirees may unintentionally work longer than necessary or miss out on experiences during their go-go years of retirement. He recalls helping a 63-year-old retiree who initially believed she could only afford to spend $4,200 per month. After building her income plan, they discovered she could safely spend $5,200. Just three years later, that number increased to $6,500—and eventually, with inflation accounted for, she could afford nearly $8,000 per month without jeopardizing her long-term financial security.

The solution to this trap is an intentional, customized income plan. This plan replicates the consistency of a paycheck during working years by blending guaranteed income sources like Social Security and pensions with scheduled withdrawals from retirement accounts. With this framework, retirees gain the clarity and confidence to spend comfortably, knowing their income supports their desired lifestyle for the long haul.

Trap #2: Overlooking the Power of Cash

Many retirees underestimate the role of cash in their retirement strategy, focusing instead on market investments. While investments remain important, an effective retirement plan must incorporate smart cash management as well.

Today’s higher interest rate environment opens new opportunities. As Loren explains, there’s a meaningful difference between keeping cash in a traditional bank account yielding 1% versus a money market account earning 4%. Both offer similar liquidity, but one works significantly harder on your behalf. Choosing the more efficient option can lead to better outcomes with minimal additional risk.

Chawn notes that this mindset shift is part of the broader evolution from an investment plan—which dominates during working years—to a comprehensive retirement plan, which encompasses six key planning areas: lifestyle, income, taxes, investments, health care, and legacy.

For instance, using taxable IRA withdrawals to fund pre-Medicare expenses can increase Medicare premiums due to higher reported income. Cash, by contrast, doesn’t count toward income thresholds and can be used strategically to avoid or lower those premiums. Loren recalls a recent case where they preserved tax flexibility and reduced Medicare costs by using cash to bridge the gap until Medicare eligibility.

Even individuals nearing retirement who don’t currently have substantial cash reserves can begin preparing now. Building up cash slowly provides greater flexibility and control during retirement’s critical early years. Over time, this approach allows retirees to manage taxes more effectively, respond to market volatility with confidence, and protect against health care cost spikes.

As Chawn concludes, well-planned cash reserves enhance multiple pillars of retirement strategy—income, taxes, health care, and investments. By leveraging this underappreciated resource, retirees gain more options and control throughout their financial journey.

Trap #3 Not Planning for Longevity

Life expectancy has seen a dramatic increase over the past century. In 1950, the average life expectancy was just 68 years. By 2024, that number has risen to 79.46 years — a clear sign of advances in health care, lifestyle, and technology.

But averages don’t tell the whole story. For many retirees, especially couples, longevity is becoming the norm:

- Half of all couples who reach age 65 will have one spouse live to at least age 93.

- 1 in 3 people turning 65 today will celebrate their 90th birthday.

- 1 in 7 will live to age 95 or beyond, according to the Social Security Administration.

Failing to plan for a long life is risky—no one wants to outlive their money; a possibility that, as Loren points out, creates significant anxiety. Planning for longevity means running income projections not just to age 80 or 90, but even to 100. This may seem excessive, but it provides a real safety net. Chawn and Loren emphasize the importance of considering Social Security optimization, building a tax plan, and planning for long-term care.

Trap #4 Mismanaging Withdrawals

Mismanaging withdrawals in retirement can lead to one of the most unexpected outcomes: paying more taxes than expected. Loren explained that even if someone has done a good job building tax diversification across different account types, it doesn’t automatically result in tax savings. Without a coordinated withdrawal strategy, retirees might take income in a way that pushes them into higher tax brackets — eroding their retirement income.

Chawn expanded on this by illustrating a common mistake: pulling funds first from taxable accounts like traditional IRAs or 401(k)s without considering the tax implications. This can cause retirees to bump into a higher tax bracket and think, “Maybe I should have used other accounts instead.”

Loren added that neglecting to use available cash reserves — which can be withdrawn with little or no tax consequences — can exacerbate the problem. Not only could this increase the retiree’s overall tax burden, but it may also raise Medicare premiums and shorten the longevity of their retirement savings.

So how can retirees avoid this trap?

Chawn stressed the importance of building and maintaining a tax-efficient income strategy. This means coordinating withdrawals across different account types — not just focusing on minimizing taxes this year, but across an entire retirement lifetime.

Loren pointed out that once a distribution plan is in motion, it’s critical to remain flexible. Retirement income strategies shouldn’t be static — they must adapt to market changes, tax law updates, and personal shifts in income needs.

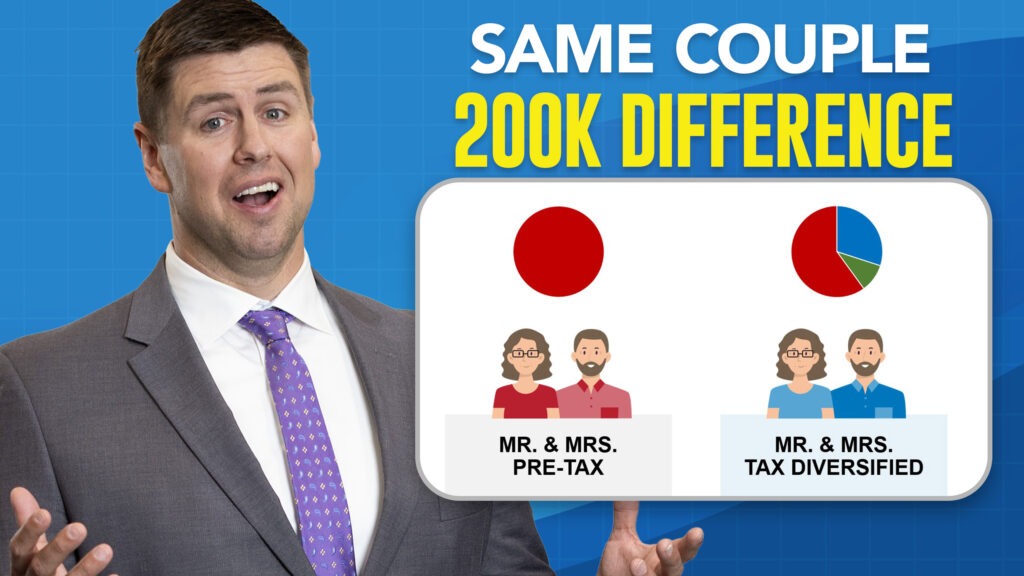

Loren explained that there are three types of retirement income “buckets”:

- Pre-tax accounts, like traditional IRAs and 401(k)s, which are fully taxable when withdrawn

- Roth accounts, such as Roth IRAs and Roth 401(k)s, which are generally tax-free

- After-tax accounts, including brokerage or savings accounts, which may only be taxed on gains

Chawn added that ideally, retirees will have access to all three. And if they don’t, part of the retirement planning process should include creating tax diversification ahead of time to maximize flexibility and efficiency later.

The bottom line? Withdrawals are about more than simply accessing savings. Done thoughtfully, they can help reduce taxes, maintain Medicare benefits, and extend the life of retirement assets.

Trap #5: Underestimating Inflation

Underestimating inflation is one of the most dangerous traps in retirement planning—and it often goes hand-in-hand with the challenge of longevity. As retirees live longer, the rising cost of living becomes a growing threat to maintaining a consistent lifestyle over time.

Loren explains the core issue: even if retirees aim to maintain the exact same lifestyle for decades, it will inevitably cost more in the future. “If you do not have an effective inflation-beating plan as a part of your overall income and retirement plan,” he explains, “you’ll eventually reach a point where your spending power is significantly reduced. By then, you’ll have fewer options to fix the problem.”

Inflation doesn’t hit all categories equally. While increases in the cost of groceries, housing, and cars are significant, inflation on health care expenses often outpaces them—sometimes by double. In the later stages of retirement, medical costs can spike dramatically, creating a serious financial burden. Chawn adds, “Health care is one of those areas that can quickly shift your expenses upward. And because it’s somewhat unpredictable, it adds a whole new layer of complexity to inflation planning.”

To avoid this trap, Loren emphasizes the importance of building inflation into your retirement plan from day one. “We use an assumed inflation rate to project spending needs over the next 20 to 25 years. That gives us a roadmap for how much income will need to grow over time.”

But it doesn’t stop there. Beating inflation requires a multi-pronged strategy. One pillar of that strategy is tax planning. As Loren puts it, “If you can send less to the IRS, you can keep more in your overall portfolio. That means more growth potential, especially when those savings are compounding.”

Another critical consideration is the Required Minimum Distribution (RMD) age. Loren refers to this as the “tax ticking time bomb.” Once retirees are mandated to begin drawing from their pre-tax retirement accounts, all those withdrawals are taxed—on top of Social Security, pension, and other income sources. Without proper planning, this can drastically increase a retiree’s overall tax burden throughout retirement.

Investment strategy is the final piece of the puzzle. Chawn highlights the need for balance: “If someone is spending $5,000 a month today, that number could easily become $15,000 in 15 or 20 years due to inflation. That’s why a portion of the portfolio must still be invested for growth.”

Even in retirement, some market risk is necessary. With the right level of diversification and asset allocation, investors can aim for strong returns when markets are up—while minimizing downside exposure.

In summary

Retirement comes with both opportunities and pitfalls. By understanding and addressing these five traps—underspending, ignoring cash, failing to consider longevity, mismanaging withdrawals, and underestimating inflation—you can help make your retirement years more flexible and fulfilling.

Click here to watch the full episode “5 Common Retirement Income Traps (And How to Avoid Them)” on YouTube!

Source: SSA.gov