Retirement planning isn’t just about saving money. It’s about making sure your plan supports the life you want to live once you stop working. Asking the right questions can uncover your goals, anticipate challenges, and create a plan that gives you and your loved ones peace of mind. Retirement Planners Loren Merkle and Clint Huntrods share seven questions your financial advisor should be asking as you head toward retirement.

What do you want to do with your free time in retirement?

It may sound surprising, but your lifestyle goals are the foundation of a retirement plan.

“Oftentimes we find that advisors are not talking to their clients about what they want to do in their free time. But this is an essential question,” says Loren.

Clint shared the story of a client whose retirement vision centered around spending time with his grandkids. For another family, it meant frequent trips from Iowa to Bozeman, Montana — until they eventually decided to move across the country to be closer to loved ones.

Lifestyle choices ripple through your financial picture — from housing to travel to taxes. That’s why Loren adds, “From a financial standpoint, it makes complete sense to start with your lifestyle.”

What’s your plan for electing social security?

Too often, families are left to figure out Social Security on their own. Some advisors may simply tell clients to elect benefits whenever they’re ready and report back later. But Social Security is far too valuable to leave to guesswork.

A married couple has up to 81 different claiming options, and the choice may potentially be worth hundreds of thousands of dollars over a lifetime, depending on your circumstances. For a single individual, benefits may add up to $500,000, while a married couple could receive as much as $1 million.

That’s why it’s important to treat Social Security like the significant asset it is — one that should be carefully coordinated with your lifestyle goals, income needs, and tax strategy. Deciding when and how to claim isn’t always straightforward, but making the right choice can be one of the most impactful parts of your retirement plan.

How will you create reliable income that lasts as long as you do?

“Just turn it on like a faucet — isn’t that easy?” Loren says when describing how some people think about retirement income. In reality, that approach leaves you with many unanswered questions: Which accounts should you draw from first? What are the tax implications? Will the amount be enough to sustain your lifestyle — and will it last as long as you do?

That’s why a written income plan is so important. As Loren explains, “It is your income roadmap… it shows you where your money’s going to come from, how much you can afford to take now and later, and how you’ll account for inflation and taxation.”

What are you planning for taxes in retirement and just before?

There’s a big difference between tax filing and tax planning. Filing is about recording history for one year. As Loren explains, “When you’re tax planning, you are looking at this current year, but you’re also looking at next year, in five years, and 10 and 15 years down the road.”

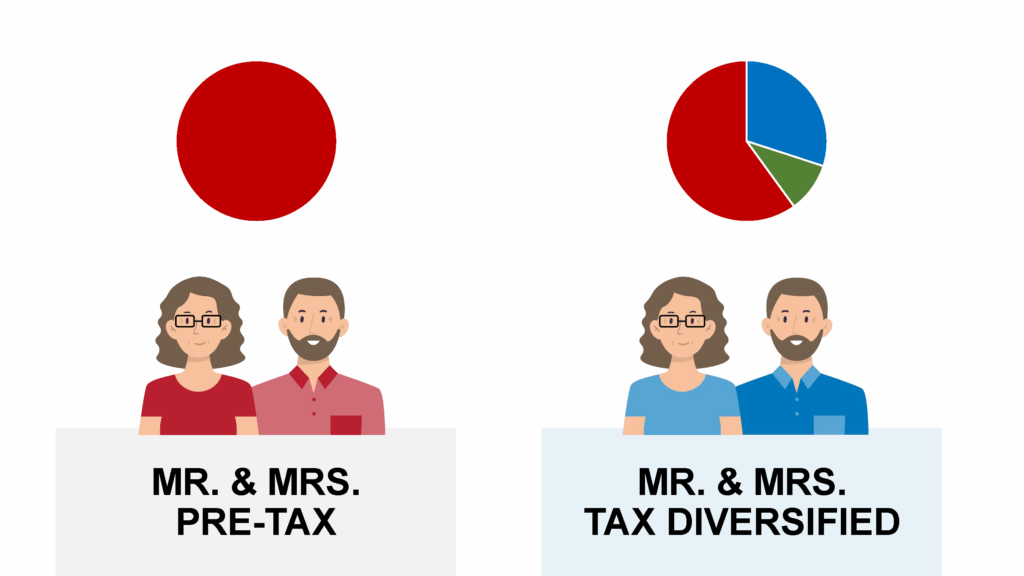

Clint illustrated the power of this proactive approach with a case study of two couples.

- Mr. and Mrs. Pre-Tax saved everything in tax-deferred accounts. Over retirement, they paid about $740,000 in taxes and passed on around $670,000 to their heirs. The problem? Half of that legacy had never been taxed, which meant their beneficiaries would owe a significant tax bill later.

- Mr. and Mrs. Tax Diversified saved more strategically, building a mix of pre-tax, Roth, and non-qualified accounts. In this scenario, their projected lifetime tax bill was just around $500,000, and in this scenario, they could leave $1.2 million — entirely tax-free — to their heirs. As Clint put it, “Their beneficiaries will not have a tax bill associated with those dollars.”

The lesson from this hypothetical example is clear: proactive tax planning can save hundreds of thousands of dollars over a lifetime and significantly improve the legacy you leave behind.

Click here to watch this example on YouTube.

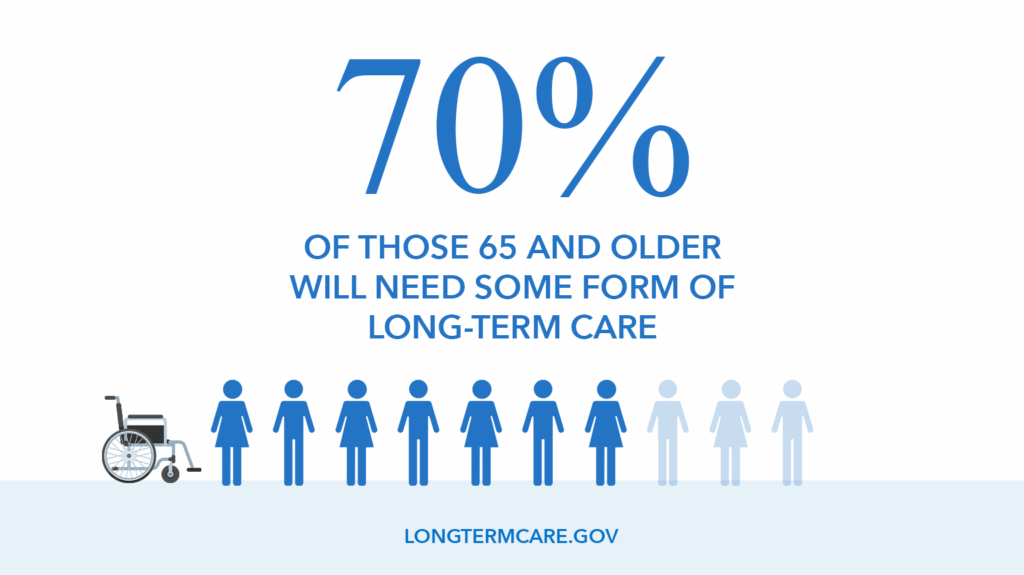

What’s your plan if you or your spouse need long-term care?

This is one of the hardest, yet most important, conversations to have. The reality is unavoidable: 70% of people age 65 today will need some form of long-term care. And the need often lasts longer than many expect — on average, women require care for 3.7 years, while men need it for about 2.2 years, according to LongTermCare.gov.

“For many people it’s not if, it’s when,” Loren says. “A lot of the times people will default to a self-insurer strategy because they don’t know what else they can do. Long-term care is really expensive, long-term care insurance is also really expensive. What most people don’t know though is there’s a lot of alternative ways you can offset the risk.”

Clint stresses that starting the conversation early matters: “The sooner you have those conversations, implement some of those strategies, the better.”

Do you have a game plan for market volatility?

Markets will rise and fall throughout retirement, but planning ahead helps you stay confident during downturns. “We know we’re going to go through a recession on average every five to six years,” Clint notes. “Let’s build in strategies to prepare for that.”

That’s where a recession-resistant portfolio comes in. As Loren explains, it’s a portfolio designed to help provide stability during market downturns. While you can’t control the markets, you can control how your portfolio is built — balancing protection on the downside with enough growth to keep up with inflation and taxes.

What’s your plan for your spouse or other loved ones if something happens to you?

Beneficiary forms are just the beginning.

“The beneficiaries are just one piece of your overall legacy plan,” Loren explains. “You need to make sure that you have a will… even if you have a mortgage on your home, a trust, a revocable living trust, is a good legacy planning strategy to help things bypass probate and go more effectively to your kids, your loved ones and your charities.”

Clint points out another benefit of planning ahead: “Now everyone can see what their retirement’s going to look like. What would happen if you needed long-term care? If someone passes away, then everybody’s on the same page.”

The Bottom line

As Loren summed it up: “There is a difference between a financial advisor and a retirement planner… If you’re using a financial advisor as you prepare for retirement or go through retirement, it could be incomplete. The retirement planner will give you the full picture.”

Asking — and answering — these seven questions will help you build a retirement plan that supports your lifestyle, protects against risks, and gives you confidence about the years ahead.

Click here to watch the full episode “7 Questions Your Financial Advisor Should Be Asking—But Probably Isn’t” on YouTube!

Sources: LongTermCare.gov