A Roth conversion can reshape your retirement tax strategy. This blog covers how it works, when it makes sense, and what to consider before making this decision.

What Is a Roth Conversion?

The basic idea behind a Roth conversion is simple: pay taxes now in exchange for tax-free growth later.

As Retirement Planner Loren Merkle explained, “What a Roth conversion is, is you have pre-tax savings. Most of you, it’s going to be in your pre-tax 401(k) or your pre-tax IRA. So this is money you’ve never paid taxes on before.”

A conversion means intentionally moving a portion of that pre-tax money into a Roth IRA and paying taxes in the year of the conversion. Loren put it this way: “You’re intentionally deciding to pay taxes now on at least a piece of that money.”

When the money moves, taxes follow. “In the year that you convert it, you do pay federal taxes at your ordinary income bracket,” Loren said, noting that some investors may owe state taxes as well.

Under current tax law, Roth conversions are generally permanent.

Why Roth Dollars Matter

Once money is inside a Roth IRA, the rules change.

Retirement Planner Clint Huntrods summed up the appeal: “Once it’s in the Roth IRA, then it’s able to grow tax-free.”

That tax-free growth can last for decades. After meeting age and timing requirements — including age 59½ and the five-year rule — qualified distributions can come out tax-free. “But once you’ve met some of those stipulations, you can take those dollars out tax-free,” Clint said. “If you don’t spend them in your lifetime, they will pass on tax-free.”

There are nuances. Withdraw too early without meeting qualified distribution rules and penalties can apply. Loren cautioned, “That penalty is 10% of whatever amount you took out that you weren’t supposed to take out.”

Another major distinction: Required Minimum Distributions (RMDs).

With a traditional pre-tax IRA, distributions are mandatory beginning at age 73 or 75, depending on birth year. “You’re mandated to take it out and then you will pay taxes on that required distribution,” Loren explained.

With a Roth IRA, there are no lifetime RMDs. “You can allow that money to continue to grow tax-free,” Loren said.

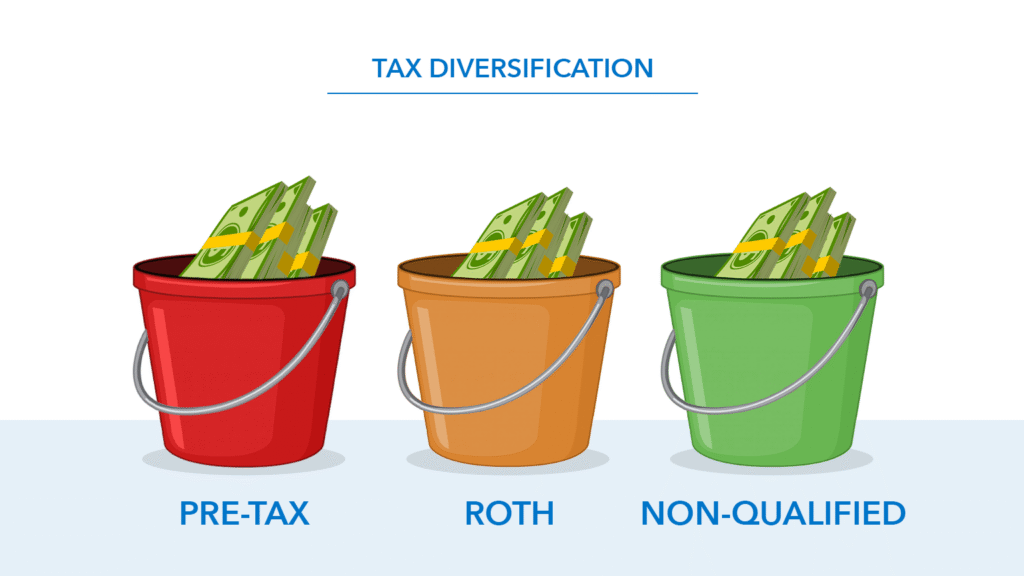

The Power of Tax Diversification

One of the strongest arguments for a Roth conversion isn’t just tax-free growth — it’s flexibility.

Clint emphasized the concept of tax diversification. “We’re used to thinking of diversification across your portfolio,” he said. “As we think more about retirement planning and your retirement plan, we want to create tax diversification.”

That means potentially having three buckets:

- Pre-tax accounts (taxed as ordinary income)

- Roth accounts (tax-free distributions)

- Non-qualified brokerage accounts (capital gains treatment)

When those buckets exist, Loren noted, “You have more control over your retirement tax bill as you go through those retirement years.”

Having options allows retirees to manage taxable income year by year, potentially staying under certain tax brackets or avoiding higher Medicare premiums. “The key with creating that tax diversification is it gives you more options, gives you more control, and has the ability then to decrease your retirement tax bill,” Loren said.

A $100,000 Example: Convert or Not?

To quantify the impact, Clint walked through a hypothetical side-by-side comparison using a $100,000 pre-tax IRA.

Scenario 1: Convert to Roth

$100,000 is converted while in the 22% bracket.

$22,000 tax bill paid upfront.

The full $100,000 grows tax-free at 6% for 25 years.

At a hypothetical 6% annual return, it could grow to $429,187.

After accounting for the $22,000 tax paid earlier, net value: about $407,187.

Scenario 2: No Conversion

$100,000 grows for 25 years at 6%.

It becomes $429,187.

At a 24% tax rate, $103,005 goes to taxes.

Net spendable amount: $326,182.

In this hypothetical example, the difference is roughly $81,005.

“That becomes really, really impactful,” Clint said. “This is just one conversion of $100,000.”

Loren acknowledged the emotional hurdle. “It is never going to feel good,” he said of paying taxes upfront, “but it’s going to feel a lot better when you know the (possible) outcome.” He added that when a planning strategy shows the potential for a meaningful long-term difference, you’re making decisions with purpose — not just reacting in the moment.

Loren also noted that many families implement multi-year conversion strategies rather than a single one-time move.

Why a Roth Conversion Isn’t for Everyone

Despite the benefits, a Roth conversion doesn’t automatically make sense.

“You will pay taxes in the year you convert,” Loren said. “Does it make sense for you in that particular year to add more taxable income to your income situation?”

Timing matters.

Clint shared that he recently worked with a family eager to convert — until deeper analysis showed they were in a higher tax bracket during their working years than they would be in retirement. “It actually didn’t make sense for them to contribute to the Roth 401(k) or to do a Roth conversion,” he said.

Loren added a critical reminder that, under current tax law: “The Roth conversion is permanent. So, once you do it, there’s not a fix. There’s not a do-over.”

That’s why it’s important to carefully evaluate the decision before moving forward.

Three Questions to Ask Before Converting

Before moving forward, there are three questions to consider.

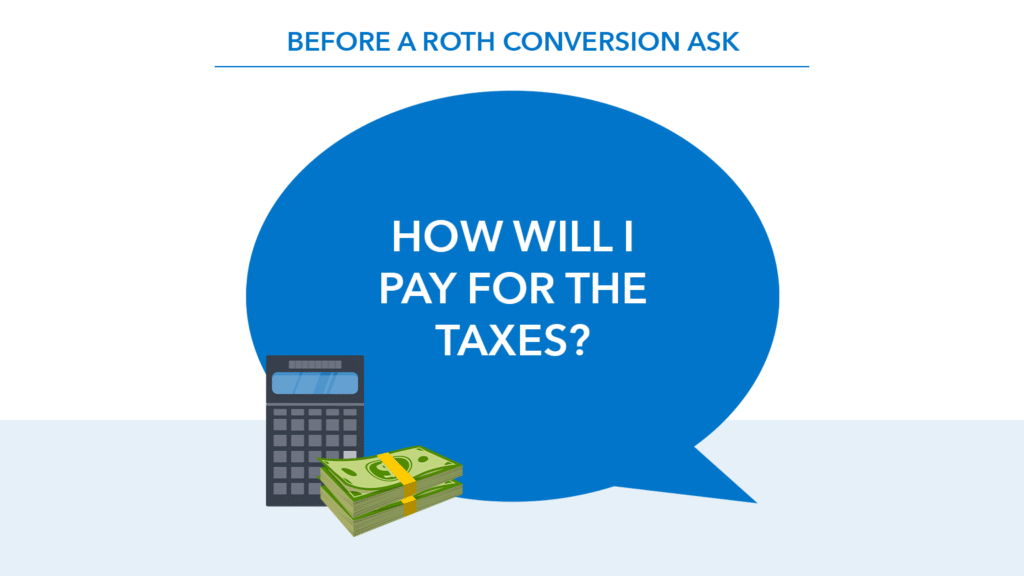

1. How Will I Pay for the Taxes?

“Do you have the money to pay the tax bill out of pocket?” Clint asked. Those over age 59½ may withhold taxes from the conversion itself, though that reduces the amount that ultimately lands in the Roth.

Clint says paying from cash reserves can preserve the full converted amount for tax-free growth.

2. Are My Tax Rates Likely to Be Higher or Lower Later?

This question often requires looking ahead.

Loren shared an example of a couple who retired at 63 and lived on cash before claiming Social Security. “We could take advantage of some conversions at really low tax rates, tax rates they haven’t seen in a very long time,” he said.

He also pointed out the broader landscape. “Right now, the lowest tax rate that we have is 10%… Right now, the highest tax rate we have available to us is 37%.” Historically, rates have been far higher; Loren adds that future legislation could change them again.

Clint described what many retirement tax projections look like: “It’s almost like the U.” Taxes may drop in early retirement years before RMDs push them back up later.

Those lower-income “window” years can create strategic opportunities.

3. When Will You Need the Money?

Time horizons are critical.

“If you’re thinking of a time horizon of two years, well, then it might not make as much sense,” Clint said. Over decades, however, “we can see how the power of that compounding growth in the Roth bucket can really impact your plan in a positive way.”

A Decision That Connects the Now and the Later

At its core, a Roth conversion is about trade-offs — paying taxes today in pursuit of flexibility, control, and potentially tax-free income tomorrow.

The numbers matter. The timing matters. And perhaps most importantly, how it fits into the larger retirement picture matters.

For some, the strategy can unlock meaningful long-term value. For others, waiting — or skipping it entirely — may be the better path.

The key is understanding which situation is yours.

Watch the full episode on YouTube and learn more about roth conversions.