If you’re offered a buyout or find yourself retiring earlier than planned, several important financial questions come into play. From health care coverage before Medicare to tax implications and 401(k) strategies, here’s what to consider as you evaluate whether early retirement is truly within reach.

When Retirement Happens Sooner Than Expected

For many workers in their 50s and early 60s, retirement doesn’t always unfold according to plan. A layoff, company restructuring, or buyout offer can suddenly shift the timeline.

Retirement Planner Loren Merkle notes that the situation has become increasingly common. “We are living in interesting times where the economy itself isn’t all that bad, but if there’s a lot of employers out there, a lot of companies out there who are asking people to leave the organization a little bit earlier than (what was) planned.”

While the experience can be stressful, having a plan can help restore a sense of control. Loren explains, “From a financial standpoint, you are prepared, you’re ready to go. And I can tell you that can go a long way to help alleviate some of the emotional stress if that day does come.”

Preparation can help make an unexpected transition feel more manageable.

Health Care Before Medicare

One of the first questions people ask when considering early retirement is how they will handle health care coverage before becoming eligible for Medicare.

Retirement Planner Clint Huntrods explains why the issue comes up so often. “The average retirement age today is about age 62. So, there’s a whole lot of people, whether they want to or are forced to, are retiring prior to being Medicare eligible.”

That gap — sometimes several years long — means retirees must find alternative coverage.

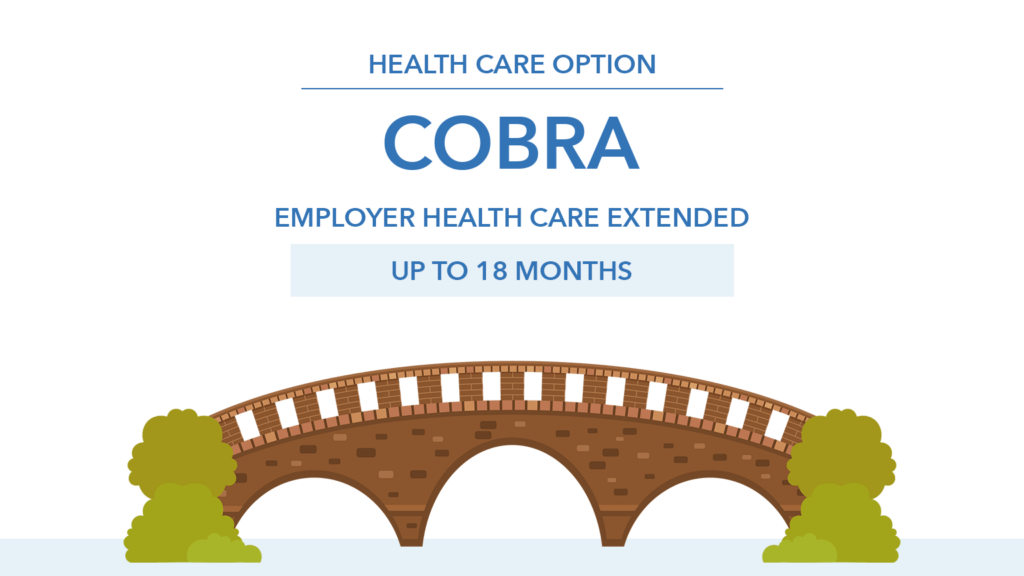

One common option is COBRA coverage through a former employer. Clint explains, “You could have continued health care from your employer, your previous employer, for up to 18 months in most cases.”

However, the cost can surprise people because the employer subsidy disappears. “Most employers pay for part of your health care cost. When you’re on COBRA, they are no longer going to pay for your health care costs.”

Another option is purchasing coverage through the health insurance marketplace. Clint adds that part of the comprehensive planning process includes comparing the cost and benefits of COBRA versus marketplace plans, since pricing and subsidies can vary based on income.

Health Savings Accounts (HSAs) can also play an important role. Clint says, “You can take money out of the HSA for qualified health care expenses and it’s tax-free. So that can be a really powerful benefit that can kind of bridge that gap between retirement timeframe and Medicare age eligibility.”

For some families, building up HSA savings during their working years becomes a valuable strategy for covering those early retirement health care costs.

Understanding the Tax Impact of Severance

If a buyout or severance package is involved, taxes quickly become another major consideration.

Loren explains that severance terms can sometimes be negotiated. “There’s some negotiating power that can really come into play based on how flexible that employer really wants to be.”

In some cases, retirees may be able to choose between different forms of compensation — such as a lump sum payout, extended salary continuation, or even additional health care coverage.

The structure matters because a lump sum payout can significantly increase taxable income in the year it’s received. “The one lump sum payment is going to be a taxable event,” Loren says.

Without proper planning, that additional income can push retirees into a higher tax bracket.

One hypothetical example highlights the consequences. A worker who deferred a $150,000 buyout payment for several years eventually received it while still employed, adding it to his household income and moving the couple from the 24% federal tax bracket to the 32% bracket.

As Clint notes, “He went from 24% federal tax bracket to 32% with $150,000 of deferred comp. That’s a $12,000 tax bill higher than what could have been.”

Planning ahead can help retirees decide whether spreading income across multiple years or restructuring a severance offer could lead to a more favorable tax outcome.

What Happens to Your 401(k)?

Another key question during an early retirement transition is what to do with workplace retirement savings.

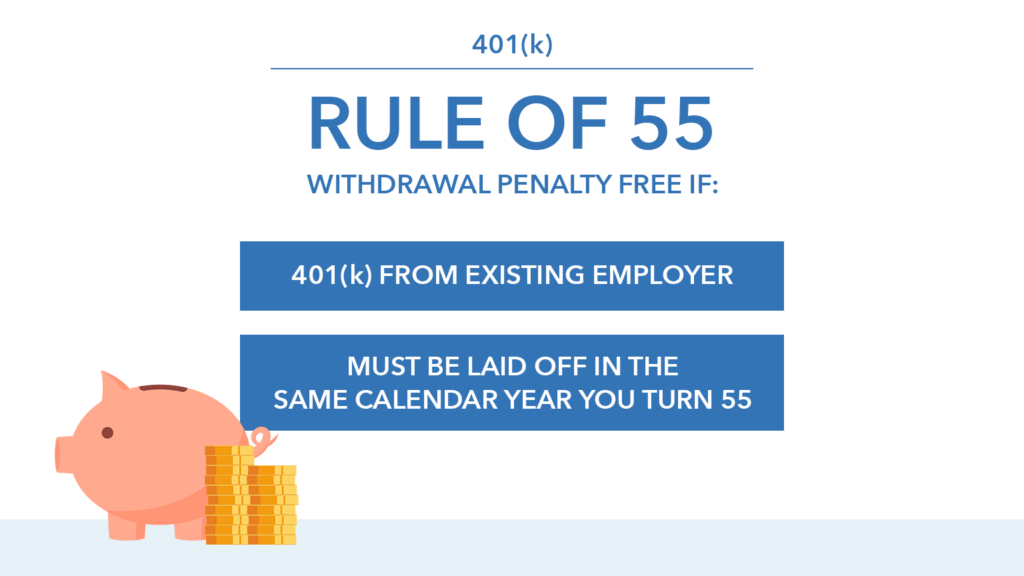

For individuals under age 59½, withdrawing from retirement accounts can trigger a 10% early distribution penalty. But there is an exception that many people don’t realize exists.

Clint explains, “If they’re 55 or older, it may make sense for them to keep their 401(k) in the plan that it’s in, and then use the rule of 55.”

This rule allows workers who leave their employer at age 55 or later to take distributions from that employer’s 401(k) plan without the early withdrawal penalty.

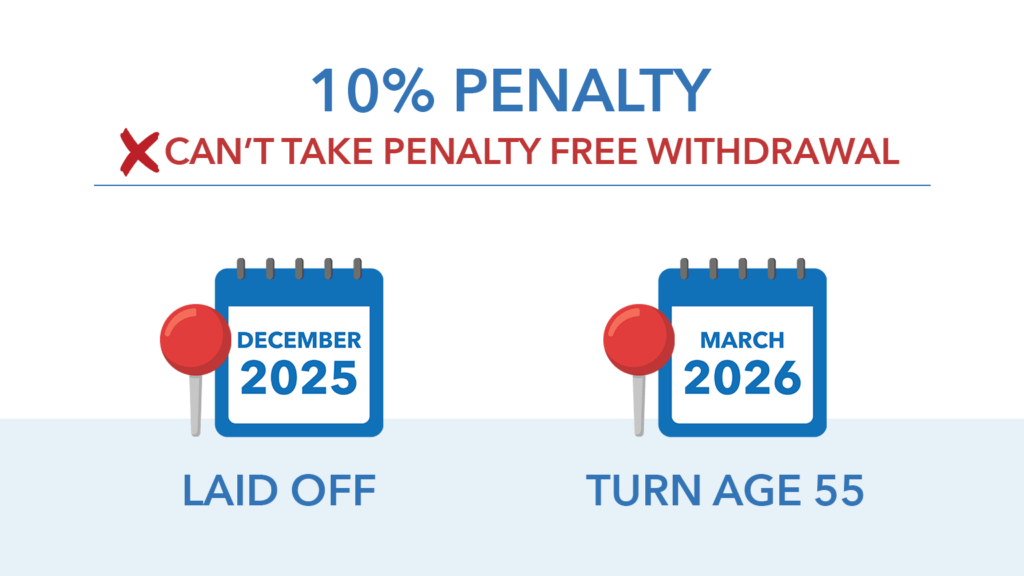

However, the rule has strict requirements. The distribution must come from the 401(k) tied to the employer where the separation occurred, and the individual must turn 55 during the same calendar year as the job separation.

Loren cautions that mistakes can be costly. “You want to make sure you’re really careful because there are a lot of rules to this.”

Even beyond the penalty rules, 401(k) plans themselves can present limitations. Clint explains that they are great for retirement savings, but when it’s time to use them for income there are things to be aware of.

Some plans restrict how often distributions can occur, while others require fixed withholding rates that may not align with a retiree’s actual tax situation.

For that reason, when planning for retirement some people choose to move funds into an IRA once they reach the appropriate age and to gain more flexibility with withdrawals and tax planning.

The Question Everyone Asks: Do I Have Enough?

For anyone facing early retirement, one question inevitably rises to the top: Do I actually have enough to retire?

Loren says it’s the most common concern among people approaching retirement. “The number one question, if you’re looking to retire within the next five years, that is top of mind for almost every single one of you.”

Answering that question requires more than estimating a single retirement number. It involves creating a comprehensive retirement plan that shows how income, taxes, health care, investments, and legacy goals work together.

As Loren explains, “You create a roadmap of a written retirement plan that is going to show you how you can accomplish your goals.”

When families see that plan mapped out, it often clarifies their options. Some may find that they are able to retire earlier than expected, while others may decide to work a few more years or shift to a lower-stress role.

Clint often sees retirees reevaluating what their later working years might look like. “Maybe they made $150,000, but you know what? They were stressed and they had management responsibilities and those were things they were looking to get away from.”

In some cases, the plan may show that a lower-paying but less stressful job can still support long-term retirement goals.

Planning Creates Flexibility

Whether retirement comes by choice or by circumstance, preparation can make the transition far less overwhelming.

Many people assume retirement planning is only about reaching a certain age or hitting a certain savings goal. In reality, it’s about understanding your options.

When workers approach retirement with a clear strategy for health care, taxes, income sources, and investment withdrawals, they gain the flexibility to handle unexpected changes — including buyouts, layoffs, or early retirement opportunities.

And in today’s workplace environment, that flexibility can be especially valuable.

Watch the full episode on YouTube and learn more about what to consider as you evaluate whether early retirement is truly within reach.