Retirement taxes can feel overwhelming, especially when income starts coming from multiple sources. This blog walks through how different retirement accounts are taxed, why those taxes can matter more once paychecks stop, and how thoughtful planning can help retirees keep more of what they’ve saved.

The Tax Reality of Retirement

Taxes don’t disappear when work ends—they can become more complicated. In retirement, income can come from multiple sources, each taxed differently. Without a clear understanding of how those pieces fit together, retirees can be caught off guard by how much they owe.

As Retirement Planner Loren Merkle explains, many people are surprised by the impact taxes can have on their retirement savings:

“You have a million dollars saved for retirement. You’re thinking, I did a good job, I saved a million dollars over the course of (my) career and now I can use that for retirement. But if it’s never been taxed before, when it comes out, it will be taxed.”

That reality can affect how much of that money may be available to spend.

Pre-Tax Accounts: A Common Starting Point

For many savers, the bulk of retirement money lives in pre-tax accounts like traditional IRAs and 401(k)s. Retirement Planner Chawn Honkomp notes why this is so common:

“Those types of accounts have been around longer. So, when you think about the pre-tax, it’s your traditional 401(k) balances, it’s your traditional IRAs… which is why most of you have a majority of your retirement funds in those pre-tax accounts.”

The benefit comes upfront, but the tradeoff shows up later. When money comes out, it’s taxed as ordinary income. Loren puts the long-term impact into perspective:

“If we look at the retirement tax bill that most million-dollar account savers have over the course of a 25-year retirement, it’s over $500,000 over the course of that time frame.”

Required Minimum Distributions or RMDs add another layer. Chawn explains that once RMDs begin, control can be limited:

“Now people have to start taking a certain percentage of those pre-tax dollars out which… get taxed. So now you’re going to owe some of that tax bill.”

After-Tax and Roth Accounts: More Control

Not all accounts are treated the same. Roth IRAs and Roth 401(k)s are funded with after-tax dollars, but the payoff comes later. Loren describes their appeal:

“You put your money in, it’s taxed… and then it grows tax free. So later down the road a qualified distribution comes out completely federally and in most cases state tax free.”

He adds why these accounts are often viewed as the most powerful in retirement planning:

“If you have a million dollars in your Roth 401(k), you may be able to access the full amount tax-free, depending on how the account was funded and the distribution rules.”

Even for those who don’t already have Roth savings, Chawn emphasizes it’s not too late:

“As long as we have a long-term tax plan… it’s never too late. You can build up that balance, give you more options later in life.”

Roth IRAs also avoid RMDs, which can help with flexibility. Loren says that flexibility equals peace of mind:

“You want the maximum amount of control over this money that you can. The Roth IRA does that for you.”

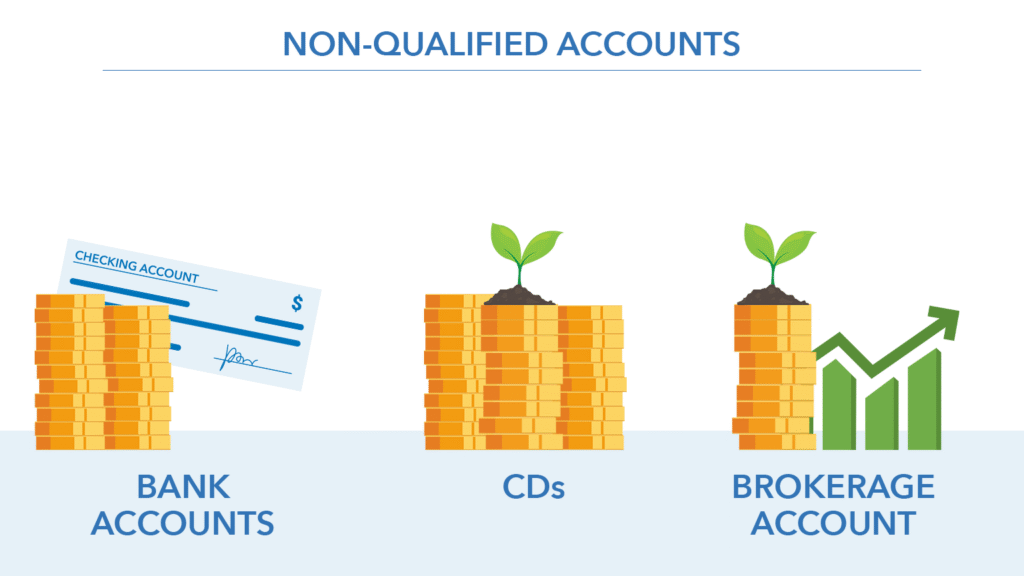

Non-Qualified Accounts and Capital Gains

Savings outside retirement plans—like brokerage or bank accounts—play a different role. Chawn explains how these non-qualified accounts are taxed:

“You don’t ever get taxed on those dollars as those non-qualified accounts grow. And when you take distributions in the future, you only get taxed on the growth of those.”

He highlights another advantage:

“When we’re taking money out of these non-qualified accounts, they can be taxed as capital gains… Now those are more favorable tax rates.”

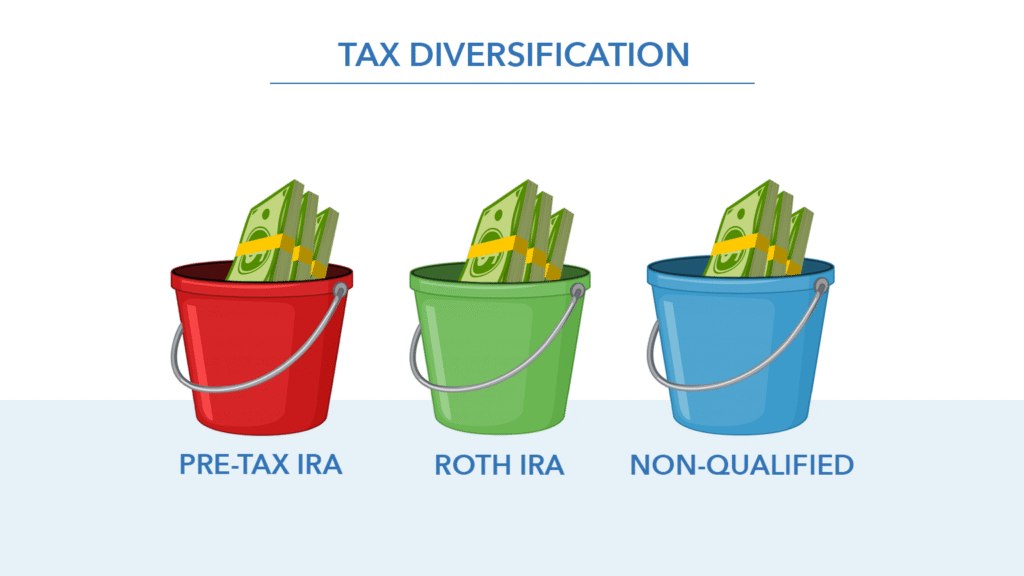

Having a mix of account types can create tax diversification, something both Chawn and Loren say can be helpful when developing a comprehensive retirement plan.

Why Tax Diversification Matters

Once paychecks stop, taxes can quietly erode income.

Chawn explains how diversification helps manage that risk:

“One of the ultimate goals is to have this tax diversification within your entire retirement portfolio so that you’ve got different dollars that are in a different tax type, which ultimately leads to control.”

With multiple buckets to draw from, income can be planned more intentionally year by year.

Social Security and Provisional Income

Social Security adds another twist. How much of it is taxed depends on something called provisional income. Chawn explains:

“How much of a person’s Social Security is subject to tax is driven by how much other income you have in a given year that is also taxable.”

Loren points out what that can mean in practice:

“It really could mean that you’re either going to pay tax, federal tax on your Social Security, or maybe you’re not.”

The difference often comes back to how diversified retirement income sources are.

State Taxes and Recent Law Changes

Taxes don’t stop at the federal level. State rules vary widely. Loren notes Iowa’s recent changes:

“At the age of 55 plus you are not taxed in the state of Iowa on any retirement income.”

That shift can represent meaningful savings over time.

Federal laws also continue to evolve. Referring to the One Big Beautiful Bill Act, Loren says:

“The implications are vast.”

One provision includes an extra deduction for certain retirees, though income limits apply. He cautions that strategies may need to adjust as laws change.

Planning Ahead Can Help Create More Flexibility

Across all account types and tax rules, one theme keeps resurfacing: time. Loren sums it up simply:

“Time is your biggest friend when it comes to any type of planning.”

Understanding how accounts are taxed and how they work together can help retirees keep more of their money and feel more confident about the years ahead.

Watch the full episode on YouTube and learn more about retirement spending.